The RFS service provides an opportunity for U.S. public companies1 to express their differences of opinion with Glass Lewis’ analysis on proxy proposals (e.g., Say on Pay proposal) to be voted on at their annual meeting. Glass Lewis will then make the feedback available to more than 3,000 individuals/entities who subscribe to Glass Lewis’ research and voting services in the form of a Report Feedback Statement. At the same time, Glass Lewis will distribute its response to a company’s RFS to its subscribers. The RFS will not be available to organizations that are not Glass Lewis clients, including the media.

The 2019 proxy season will serve as a pilot for the RFS service, which Glass Lewis will make available to a limited number of U.S. public companies. Glass Lewis intends to broaden participation after the 2019 proxy season, including introducing the service across several markets globally.

The following Q&As describe the key elements of Glass Lewis’ RFS service:

What is the deadline for submitting an RFS?

A company must submit a Report Feedback Statement within four business days following Glass Lewis’ publication of the company’s Proxy Paper report. Additionally, at least 30 days before its annual meeting, a company must enroll in Glass Lewis’ free Issuer Data Report (IDR) program and complete the IDR within two days of publication of the Glass Lewis Proxy Paper report. The IDR program provides a company the opportunity to correct errors found in some of the data that Glass Lewis includes in its company report.

Is there a cost to participate in the RFS service?

Yes. A public company must pay the following fees to participate in the RFS service:

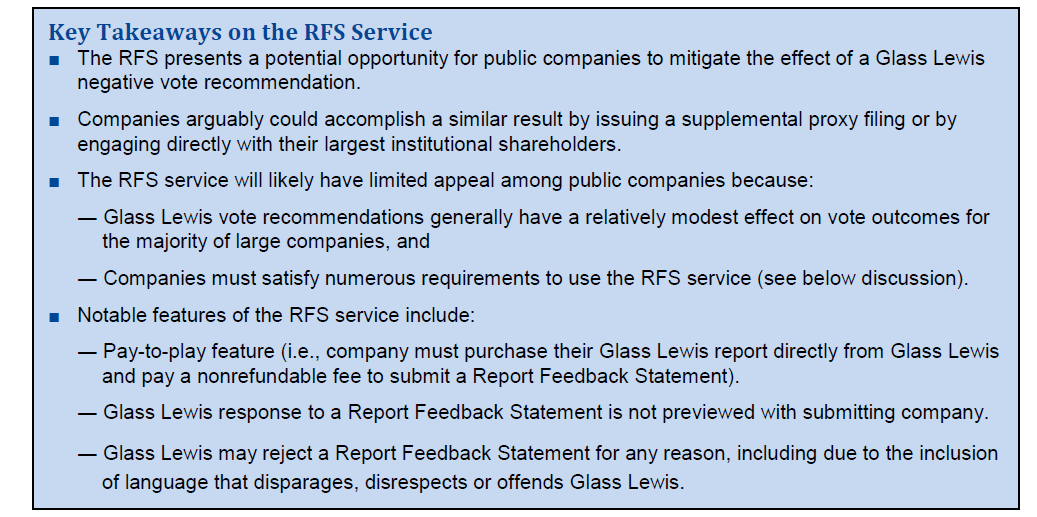

■ Fee to purchase Glass Lewis report on company’s proxy proposals:

― S&P 500 companies: $5,000

― Russell 3000 companies: $3,500

― All other companies: $750

■ Fee to submit Report Feedback Statement: $2,000

A company must purchase its Glass Lewis report in advance of submitting an RFS. The fee to purchase the Glass Lewis report is nonrefundable, even if a company decides not to submit an RFS.

Are there limits to the number of U.S. public companies that may participate in the pilot RFS service?

Yes. Under the pilot program from March through May 2019, Glass Lewis will cap the number of U.S. public companies that may participate in the RFS service at a maximum of 12 companies and/or shareholder proponents per week. The weekly cap is subject to change depending on the length and complexity of the statements received for any week.

Are there specific requirements that an RFS must satisfy?

Yes. To pass muster with Glass Lewis, an RFS and the submitting company must meet the following requirements:

■ A Report Feedback Statement must:

― be submitted under the company’s letterhead and include contact information to enable investors to follow up with the organization,

― include only “publicly available” information,

― exclude statements that defame, disparage, disrespect or offend Glass Lewis, its subsidiaries, owners, and employees, or any third party,

― exclude statements relating to the views, analysis or vote recommendations of other proxy advisors,

― exclude comparative analysis between the research published by Glass Lewis and the research published by another proxy advisor,

― exclude statements that exclusively identify factual errors in the Glass Lewis report (as Glass Lewis has a separate mechanism for reporting such errors), and

― be signed by an executive who is an authorized representative of the submitting company, with the authority to issue external statements on behalf of the company.

■ A submitting company must also:

― consult with legal counsel to ensure the submission of its RFS complies with Regulation FD and any other regulatory requirements applicable to the company and its disclosure of information,

― identify the names of shareholder proponents in the company proxy for any shareholder proposals up for vote at the relevant meeting,

― make a good faith effort to ensure that all the information contained in the RFS is accurate,

― notify Glass Lewis of any potential errors or omissions in the Glass Lewis report within two business days of the initial publication of the report,

― participate in Glass Lewis’ free IDR program and complete the IDR process prior to the company submitting its RFS, and

― execute the RFS terms and conditions.

Glass Lewis also reserves the right, in its sole discretion, to accept or reject an RFS for any reason.

Will Glass Lewis issue a response to a company’s RFS?

Yes. Glass Lewis will develop a response to comments and issues raised in a company’s RFS. Glass Lewis presents to investor clients both the RFS and its response to the statement. However, Glass Lewis will not preview its response to companies that submit Report Feedback Statements.

Meridian Comments. Glass Lewis’ new service encouraging public company feedback appears to be a departure from its long-standing policy of avoiding engagement with public companies during a company’s solicitation period.2 Glass Lewis takes a rather dim view of such engagement noting on its website that “issuers generally try to use solicitation-period discussions to lobby for support of a recommendation or to learn what changes Glass Lewis requires in order to win Glass Lewis support for items up for vote.” Therefore, Glass Lewis “avoids off-the-record discussions with companies during the solicitation period to ensure the independence of [its] research and advice…”

Although the RFS service does not allow public companies to engage Glass Lewis, the service provides public companies an outlet to respond to Glass Lewis vote recommendations and potentially persuade investors to support their proxy proposals. However, Glass Lewis will have the final word regarding any company feedback. Many companies may find this feature unappealing, along with the lengthy list of requirements that must be satisfied for participation in the RFS service.

We doubt many companies will utilize the RFS service. Unlike Institutional Shareholder Services (ISS), whose vote recommendations (particularly on Say on Pay proposals) often have a material impact on voting results, Glass Lewis typically has less impact on vote results. Therefore, we believe that the RFS service will appeal to a relatively narrow group of companies that meet the following criteria:

■ In the current proxy year, Glass Lewis has issued an adverse vote recommendation on one or more management proposals and management believes such vote recommendation is inappropriate and will likely depress favorable votes on the proposal.

■ Management believes that submitting a Report Feedback Statement is the best and most efficient manner in which to rebut an adverse Glass Lewis vote recommendation.

As an alternative to using the RFS service, we anticipate companies that choose to respond to an adverse vote recommendation from Glass Lewis and/or ISS will continue to do so through a supplemental proxy filing or by engaging directly with their largest institutional shareholders.

The RFS service is part of a broader evolution of Glass Lewis’ interactions with public companies, which include its direct engagement with companies outside of the proxy solicitation period, its IDR program and its portal for reporting errors and inaccuracies in its reports. Glass Lewis seems to be trying to counter some of the criticisms that public companies and business organizations have raised about proxy advisory firms at a time when regulation of the proxy advisory firms appears imminent. However, Glass Lewis’ recent initiatives are unlikely to ameliorate concerns of companies and regulators about the role and influence of proxy advisory firms.

1 RFS services will also be available to shareholder proposal proponents. However, this client update solely discusses the applicability of RFS services to public companies.

2 A company’s “solicitation period” begins on the date the company sends notice of its annual meeting to shareholders and ends on the date of the meeting.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com