The White House issued President Trump’s proposal on tax reform entitled “Unified Framework for Fixing Our Broken Tax Code.” The tax proposal provides slightly more details than the one issued in July, but remains a work in progress. The President has left it to the House Committee on Ways and Means and the Senate Finance Committee (“House and Senate Committees”) to fill in the blanks.

Despite eager anticipation a across Corporate America for the President’s tax proposal, passage of something near to its current form remains uncertain.

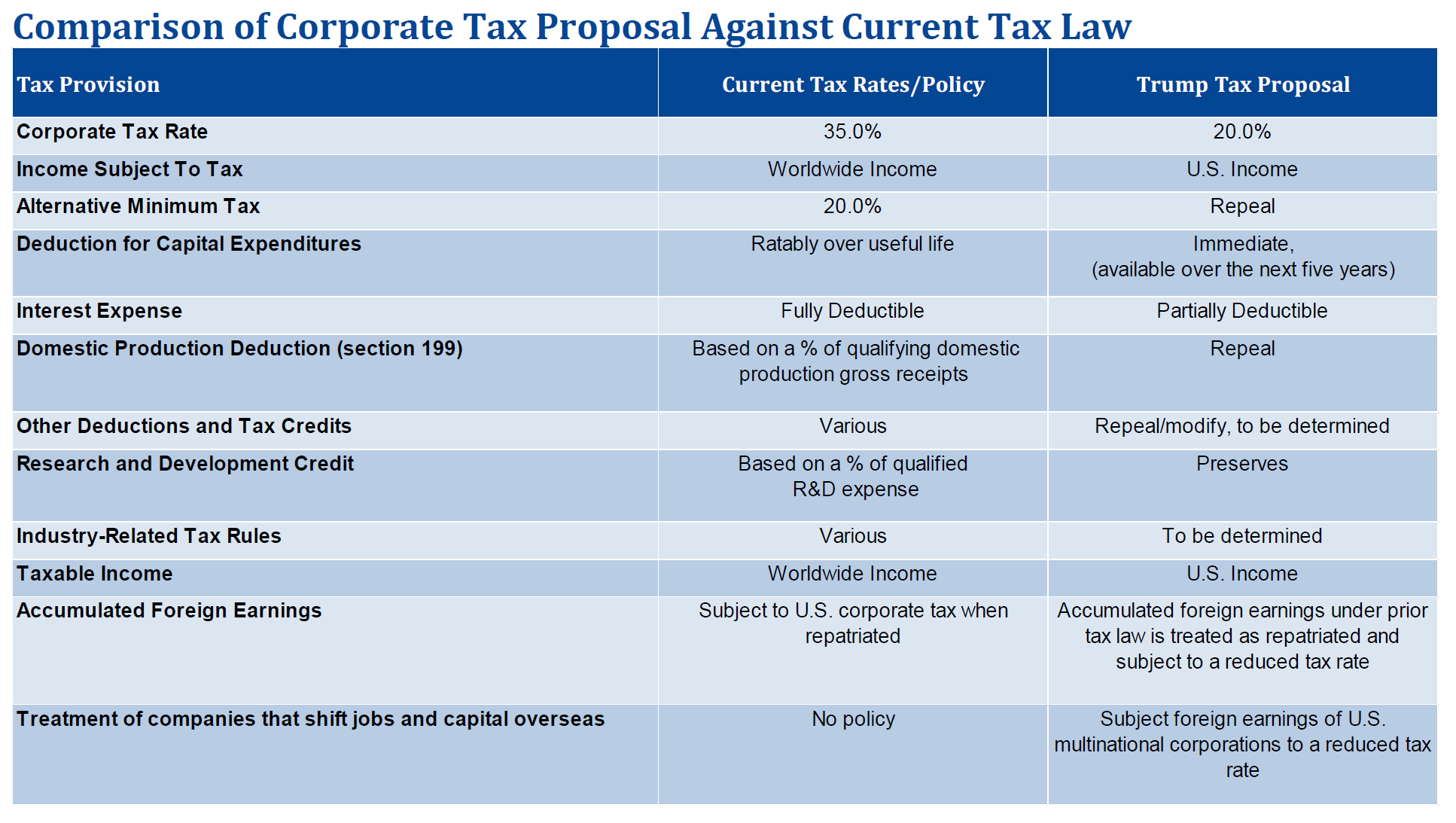

Proposal on Corporate Income

The following are the key elements of the President’s corporate tax proposal.

■ Substantial reduction in corporate tax rate. The tax rate on corporate income would fall to 20% from 35%.

■ Elimination of the Corporate Alternative Minimum Tax (AMT). Corporate AMT would be eliminated.

■ Acceleration of deduction for capital investments. Businesses would be allowed to immediately deduct the cost of new investments in depreciable assets (other than structures) made after September 27, 2017, rather than amortize the cost over the assets’ useful life. This accelerated deduction of capital investments would be available for at least five years.

■ Partial limitation on deduction for interest expense. The deduction for net interest expense incurred by C corporations would be partially limited by a yet to be determined amount.

■ Treatment of other business deductions and credits.

― Elimination of domestic production (“section 199”) deduction

― Elimination or restriction of yet to be identified special exclusions, deductions and tax credits

― Preservation of at least two tax incentives: (i) research and development (R&D) and (ii) low-income housing

■ Tax rules affecting specific industries. Modernization of industry specific tax rules to ensure that the tax code better reflects economic reality and that such rules provide little opportunity for tax avoidance. The tax proposal provides no other details on this call for modernization of industry specific tax rules.

■ Move to territorial tax system. Corporate earnings subject to tax would be limited to U.S.-derived income. Currently, a U.S. corporation’s worldwide earnings are subject to taxation. The proposal would exempt from taxation dividends derived from foreign subsidiaries (in which the U.S. parent owns at least a 10% stake).

■ Treatment of accumulated foreign earnings. The tax proposal would treat foreign earnings that have accumulated overseas under the prior tax code as repatriated and would subject these earnings to a yet to be determined reduced tax rate. The payment of this tax liability would be spread over several years.

■ Treatment of companies that ship jobs and capital overseas. To prevent companies from shifting profits to tax havens, the tax proposal would tax at a reduced rate foreign profits of U.S. multinational corporations. The tax proposal directs the House and Senate Committees to draft rules to level the playing field between U.S.-headquartered parent companies and foreign-headquartered parent companies.

Meridian Comment. As we noted in our Client Update covering the White House July 2017 tax proposal, the proposed dramatic reduction in corporate tax rates and the move to a territorial tax system could profoundly affect companies’ performance plans linked to net income, earnings per share or any other post-tax measure. According to a Wall Street Journal article, a Bank of America Merrill Lynch study concluded that S&P 500 companies would see a 12% increase in earnings per share based on a 20% tax rate and the U.S. moving to a territorial tax system.1

We also observed in that Client Update that often performance awards expressly provide that the determination of achieved performance exclude the effect of substantial change in tax laws. Depending on the specific plan design, these awards would not be affected by enactment of President Trump’s proposed tax plan. However, where a plan is silent, Boards and Compensation Committees will need to evaluate whether, and to what extent, any positive (and, in some cases, negative) effect of tax law changes on achieved performance should be considered. When companies develop incentive performance metrics for annual or long-term performance awards, they should address the potential tax impact on certain financial metrics, such as net income or earnings per share.

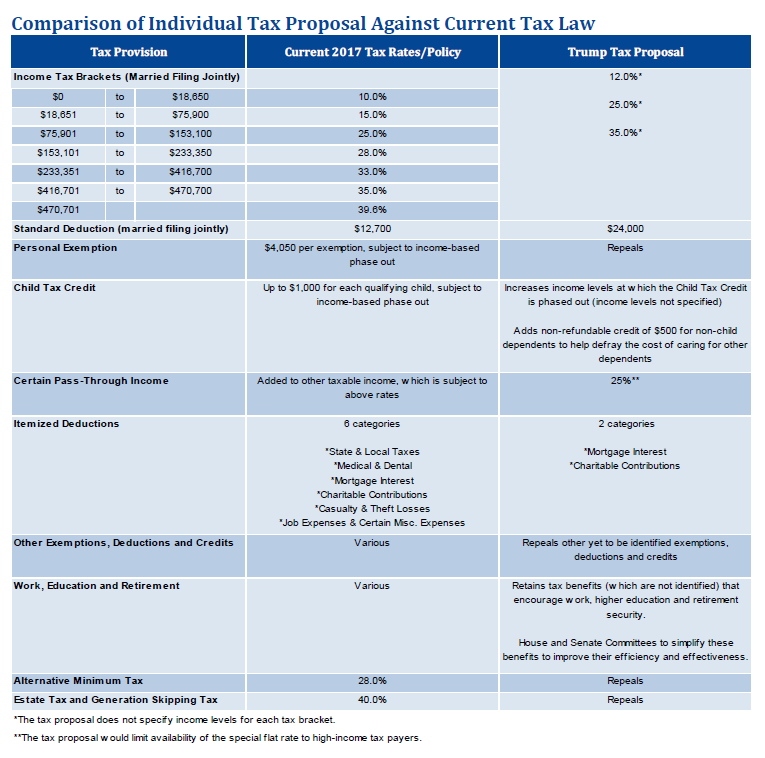

Proposal on Individual Income

The following are the key elements of the President’s individual tax proposal.

■ Reduction in number of tax brackets and top marginal rate. The number of tax brackets would fall to three from seven and the top marginal rate would fall to 35% from 39.6%. The three marginal rates would be 12%, 25% and 35%. However, the proposal does not identify income levels for each tax bracket. In addition, the tax proposal contemplates the possibility of adding a new higher tax bracket “to ensure that the reformed tax code is at least as progressive as the existing tax code and does not shift the tax burden from high-income to lower- and middle-income taxpayers.”

■ Elimination of most itemized deductions. The tax proposal would retain deductions for mortgage interest and charitable contributions and would eliminate all other itemized deductions (e.g., real estate taxes paid, State and local taxes paid, casualty and theft losses).

■ Increased standard deduction. The standard deduction for a married couple filing jointly would almost double to $24,000 from $12,700. For a single taxpayer, the standard deduction would be $12,000. The proposal would eliminated personal exemptions.

■ Elimination of alternative minimum tax (AMT). AMT would be repealed.

■ Elimination of other exemptions, deductions and credits. Other yet to be identified exemptions, deductions and credits for individuals that “riddle the tax code” would be repealed.

■ Elimination of estate tax and generation-skipping transfer tax. The estate tax and generation-skipping transfer tax would be repealed.

■ Enhancement to Child Tax Credit and Middle Class Tax Relief. The tax proposal would broaden the availability of the Child Tax Credit by increasing the income levels at which the Child Tax Credit begins to phase out. The proposal does not specify the increased income levels. The proposal would also provide a non-refundable credit of $500 for non-child dependents to help defray the cost of caring for other dependents. The tax proposal directs the House and Senate Committees to work on additional measures to reduce the tax burden on the middle-class.

■ Introduction of new special tax on pass-through business income. Currently, income from pass-through entities (e.g., partnership income, Sub S income) is treated like wages for tax purposes. That is, such income is subject to the same marginal tax rates applicable to W-2 wages. Under the tax proposal, a special 25% flat tax would apply to “business income” derived from a pass-through entity. The House and Senate Committees are directed to write rules to prevent the characterization of personal income into business income to prevent wealthy individuals from avoiding the top personal tax rate.

■ Retention of tax benefits related to work, education and retirement. The tax proposal would retain tax benefits (which are not identified) that encourage work, higher education and retirement security. The tax proposal encourages the House and Senate Committees to simplify these benefits to improve their efficiency and effectiveness.

Unlike the President’s July 2017 tax proposal, the current proposal does not include proposed changes to capital gain tax or tax on dividends.

Meridian Comment. The proposed 25% tax rate on pass-through business income (and on income derived by sole proprietorships) appears to be among the more controversial and complex aspects of the President’s tax proposal. The tax proposal directs the House and Senate Committees to write rules to distinguish between personal compensation income and business income earned under a pass-through entity. The former would be subject to the progressive tax rates while the latter would be subject to the flat 25% tax rate.

The next two pages show side-by-side comparisons of the Trump administration tax proposal against current tax law.

1 Francis, Theo and Rubin, Richard, Companies Dig Into Details of Proposal, Wall Street Journal, April 27, 2017, p.A4.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com