Generally, the changes made to the Internal Revenue Code (“Code”) under the Tax Act are effective for taxable years beginning after December 31, 2017. The changes to the corporate income tax provisions are permanent. However, most changes to individual income tax provisions (including changes in income tax rates) are temporary and will sunset at the end of 2025.

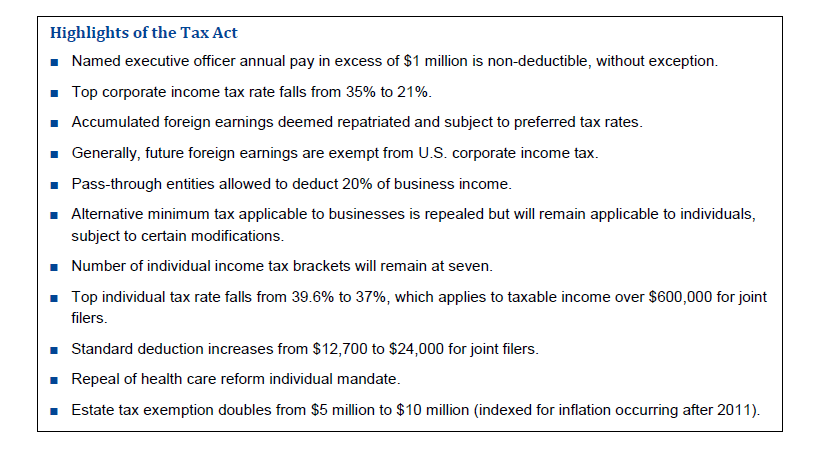

This Client Update first summarizes the Tax Act’s provisions relating to executive compensation and then compares current law and the key provisions of the Tax Act.

Provision Relating to Executive Compensation – Modification to Code Section 162(m)

The Tax Act affects only one provision of the Code that directly relates to executive compensation, Code Section 162(m) (which solely applies to “publicly held corporations”). The Tax Act makes the following modifications to Code Section 162(m):

■ Eliminates the performance-based exception to the $1 million deduction cap,

■ Expands the definition of a covered employee to include a publicly held corporation’s CFO, and

■ Provides that once an individual qualifies as a covered employee of a corporation, the $1 million deduction cap would apply to that person so long as the corporation pays remuneration to such person (or to any of that person’s beneficiaries).

Under current law, publicly held corporation refers to (i) any corporation issuing any class of common equity securities required to be registered under section 12 of the Securities Exchange Act of 1934 and (ii) any foreign corporation issuing American Depository Receipts (ADRs) subject to this registration requirement. The modification to Code Section 162(m) expands the definition of publicly held corporation to include (i) any foreign corporations issuing ADRs regardless of whether the ADRs are subject to registration and (ii) any privately held corporation required to register equity securities or debt securities.

The modifications to Code Section 162(m) will become effective for taxable years beginning after December 31, 2017 (“Effective Date”).

Transition Rule

The Tax Act also incorporates the transition rule included in the Senate tax reform bill. Under the transition rule, the modifications to Code Section 162(m) will not apply to compensation paid to a covered employee if the following conditions are met:

■ Compensation is paid under a written binding contract which was in effect on November 2, 2017, and

■ Such contract was not materially modified on or after that date.

The deductibility of compensation grandfathered under the transition rule would be determined under the current provisions of Code Section 162(m).

The written binding contract requirement may prove problematic for many common incentive plan designs. As suggested in the conference committee summary to the Tax Act, the binding contract requirement might not be met in cases where (i) amounts payable under an incentive plan are subject to company discretion or (ii) the company has the right to amend materially the plan or terminate the plan (except on a prospective basis before any services are performed with respect to the applicable period for which such compensation is paid). A company’s right to unilaterally adjust awards or amend/terminate an incentive plan suggests that the plan or awards thereunder are not subject to a binding contract but are illusory in nature.

Compliance with the written binding contract requirement will depend upon a plan’s or award’s specific terms and conditions. For example, an annual incentive plan typically allows for the compensation committee to make discretionary adjustments to otherwise earned awards. In such a case, the annual incentive plan might not be considered a written binding contract. Conversely, performance-based equity awards are typically subject to anti-cutback provisions, which prohibit the diminution of benefits under such awards without participant consent. In this case, the performance-based equity awards would appear to meet the written binding contract requirement.

We anticipate that future treasury regulations will provide clarity on the written binding contract requirement.

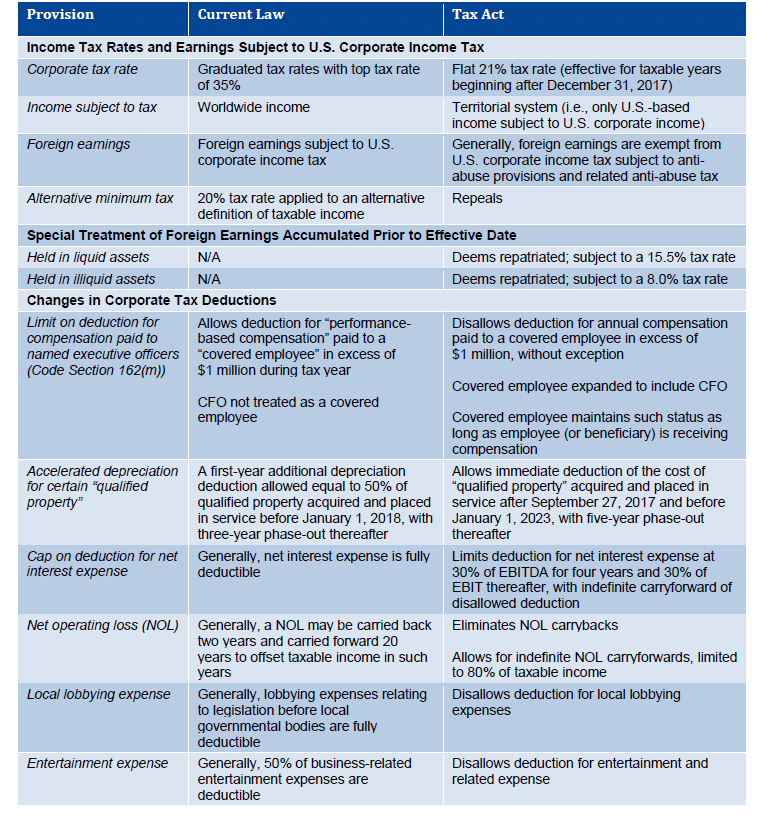

Comparison of Select Corporate Income Tax Provisions under Current Law and the Tax Act

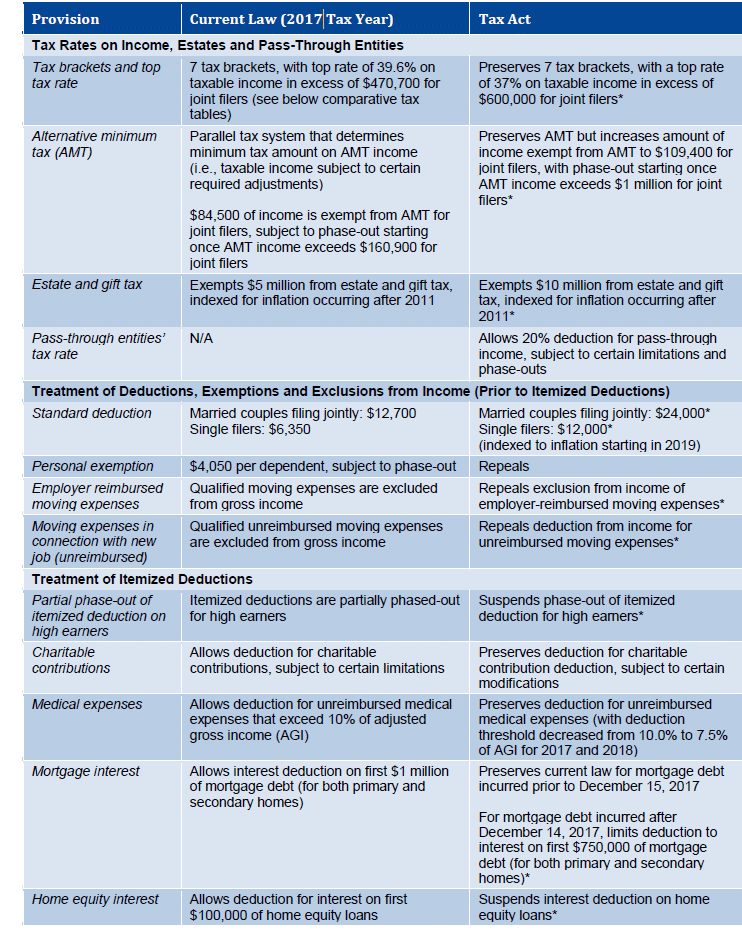

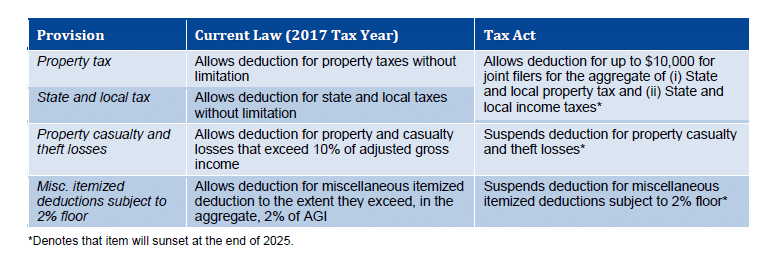

Comparison of Select Individual Income Tax Provisions under Current Law and the Tax Act

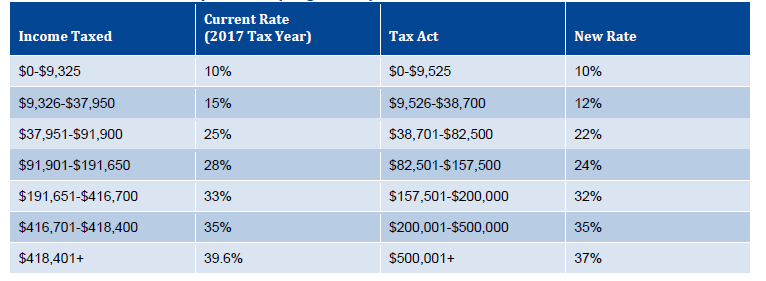

Tax Brackets for Ordinary Income (Single Filer)

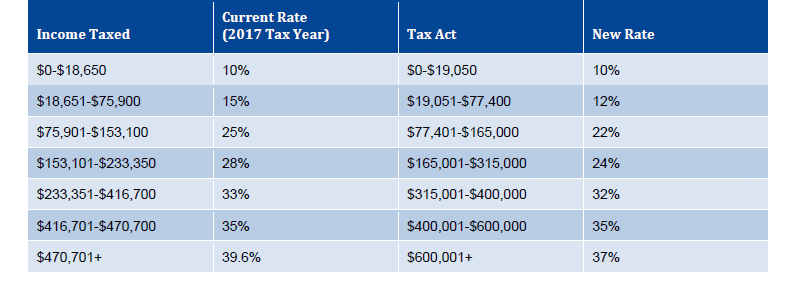

Tax Brackets for Ordinary Income (Married Filing Jointly)

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com