These proposed updates would modify ISS proxy voting policies for U.S.-listed companies as follows:

■ The quantitative pay-for-performance assessment1 would replace the currently used GAAP-based metrics with Economic Value Added (“EVA”) metrics, and

■ A board gender diversity policy that would impact ISS vote recommendations on Board members responsible for the selection and nomination of future board members.

If adopted by ISS, the policy update regarding the ISS quantitative pay-for-performance assessment would take effect on February 1, 2019 and the new policy on board gender diversity would be effective on February 1, 2020 (a grace period is provided in 2019).

Issuers and investors may submit comments via e-mail (policy@issgovernance.com) on the proposed policy updates to ISS no later than November 1, 2018. All comments received will be published by ISS, unless otherwise requested in the body of the e-mail submission.

ISS will release final 2019 policies in mid-November 2018.

Proposed Assessment of EVA Metrics in Place of GAAP-Based Metrics

ISS is proposing to modify the relative financial performance analysis (FPA) component of its quantitative pay-for-performance assessment by replacing the current financial measures with measures based on economic value added. EVA is an economic profit measure that differs from conventional GAAP-based performance measures in a number of key ways, which are discussed below.

Current Policy

Currently, ISS’s pay-for-performance evaluation for Russell 3000 companies includes a three-part comparative quantitative analysis of CEO total pay and company performance, as measured in absolute terms and relative terms (i.e., relative to an ISS-constructed peer group). A company that receives either a “cautionary low” or a “medium” level of concern on these initial quantitative pay-for-performance tests will be subject to ISS’s Financial Performance Assessment (“FPA”). Under the FPA, ISS measures a company’s financial performance based on the three-year weighted average of three or four ISS-selected GAAP-based financial metrics.

ISS uses the FPA result to modify its overall quantitative test concern level. Specifically, ISS adjusts upwards the overall concern level of a company that receives a “cautionary low” concern if the company demonstrates poor performance based on the FPA evaluation (“elevated concern”) and adjusts downwards the overall concern level of a company that receives a “medium” concern if the company shows strong financial performance based on the FPA evaluation (“mitigated concern”). A company that receives a “medium” or “high” overall concern level under the quantitative tests is subject to a more in-depth qualitative pay-for-performance assessment.

Based on the outcome of its pay for performance evaluation, ISS could issue a negative vote recommendation on a company’s say on pay proposal.

Proposed Policy

Effective for the 2019 proxy season, ISS proposes to revise its FPA to replace unadjusted GAAP financial measures with EVA-based measures. Specifically, the FPA would include the following modifications:

Whereas ISS currently uses GAAP-based FPA measures that differ by industry and/or are weighted differently by industry, ISS proposes to use the same EVA metrics, with equal weighting, for all companies across all industries. Under the proposed methodology, ISS would continue to use the FPA, as modified, for companies that receive a “cautionary low” or a “medium” concern on the initial quantitative pay-for-performance evaluation to determine a final quantitative pay-for-performance concern level.

Background on EVA

Described below is the manner in which EVA differs from conventional GAAP-based performance measures.

- EVA relies on adjusted financial data, sometimes incorporating assumptions. The intent is to remove accounting distortions in order to represent a company’s economic performance more accurately. For example, under an EVA-based approach, certain expense categories – like R&D expense – are capitalized and moved onto the balance sheet.

- EVA incorporates a charge for the cost of capital. Most fundamentally, economic profit models like EVA acknowledge that capital has a cost, and they measure performance on that basis. The inclusion of this charge allows for an evaluation of whether companies are theoretically creating or destroying value.

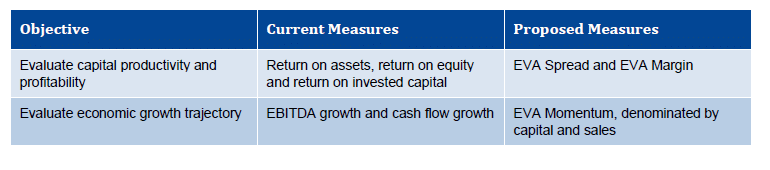

- EVA-based performance measures are fundamentally different from traditional financial measures. For example, instead of measuring profit (e.g., EBITDA) or returns generated by the business (e.g., return on assets, equity or invested capital), EVA measures net operating profit after-tax, net of a charge for the cost of capital.

Meridian Comment. As a rationale for the proposed change in the FPA component of its quantitative pay-for-performance test, ISS claims the modification will simplify the application of the FPA and enhance the comparability of FPA across companies, industries, operating models, capital structures and business cycles. ISS further states, “[t]he intent is to align the [FPA] measures with the long-term interests of shareholders by replacing accounting-centric measures with economic-centric measures.”

ISS’s proposed modification to the FPA runs counter to investor preferences as reported in the results of ISS’s recent policy survey. As we noted in our Client Update dated October 15, 2018, the results of ISS’s 2019 Policy Survey indicated investor preference is for ISS to continue to use accounting-centric metrics for FPA, rather than use EVA-based metrics. As we also noted in our Client Update dated August 15, 2018, this potential change to the ISS quantitative pay-for-performance methodology follows ISS’s recent acquisition of EVA Dimensions, a firm that measures and values corporate performance based on the EVA framework. We suspect the focus on EVA may be due, in part, to an ISS strategy to sell EVA consulting services to public companies through EVA Dimensions.

In advance of the company’s annual meeting and ISS’s proxy analysis, ISS will provide EVA data free of charge, including EVA metric results, basic benchmarking data and selected data points. ISS has not confirmed that it would provide sufficient EVA data on a subject company’s industry peers or the FPA thresholds for elevated concern and mitigated concern. Consequently, the use of EVA in the FPA may make the ISS quantitative pay-for-performance test outcome insufficiently transparent for a company to replicate independently and, therefore, result in unpredictability.

ISS expects that the new FPA methodology will have approximately the same impact as that of the current FPA methodology (i.e., ~5% of companies with a “Low Concern” should have their concern level changed to “Medium Concern” based on FPA findings). The practical impact of this change could therefore be limited.

In general, comprehensive financial performance measurements should include metrics that cover the balance sheet. In addition, understanding a company’s financial returns relative to its cost of capital is important, and incentive compensation decisions should ideally be made with this understanding in mind.

However, EVA is complicated. Few companies use it as a formal incentive plan metric. Those that do tend to be “EVA companies” – the measurement system intersects with everything the company does, and the training and cultural commitments to the system are extensive. We expect that many companies will treat the new ISS FPA as a “black box,” and we do not expect usage of EVA by companies or investors to accelerate based on this change.

Moreover, there are some industry sectors where EVA simply does not work well – notably financial services, where much of the balance sheet is fungible financial capital, and the entire business model is built on the idea of earning a positive spread on that capital. Therefore, the utility of EVA’s application in such a sector may be of limited value.

Board Gender Diversity

ISS proposes to phase-in a new policy on board gender diversity.

Current Policy

Under ISS’s current proxy voting guidelines, ISS has adopted a principle that a board “should be sufficiently diverse to ensure consideration of a wide range of perspectives.” To that end, in its proxy research report, ISS will identify when a company’s board lacks any female directors. However, ISS does not use the lack of board gender diversity as a factor in its vote recommendations on directors or on any other matter.

Proposed Policy

Effective for the 2020 proxy season (i.e., meetings held on or after February 1, 2020), ISS proposes that it will recommend AGAINST the nominating committee chair (or other directors who are responsible for the board nomination process on a case-by-case basis) if a company does not have any female directors serving on its board of directors, absent mitigating factors. This policy would be solely applicable to component companies of the Russell 3000 or S&P 1500 indices.

Under the proposed policy, the following factors may mitigate ISS concern regarding lack of board gender diversity:

■ A firm commitment to appoint at least one female director to the board in the near term (before the next annual meeting), as disclosed in the proxy statement and/or other SEC filings,

■ The presence of at least one female director on the board at the immediately preceding annual meeting (i.e., the female director is not a member of the board at the current annual meeting), and/or

■ Any other compelling factors considered relevant on a case-by-case basis.

Meridian Comment. ISS estimates that the proposed policy on board gender diversity would affect approximately 10% of Russell 3000 companies at the time of its implementation in 2020, In line with ISS’s proposed policy, we expect that investors will increasingly focus on the gender composition of corporate boards in proxy voting and issuer engagement. As such, companies should consider enhancing their respective proxy disclosures on its board composition to explain why the current board includes an appropriate mix of individuals, the factors considered in director nominations and refreshment, and actions taken to improve board diversity.

1 The proposed change to the quantitative pay-for-performance assessment also applies to Canadian companies.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com