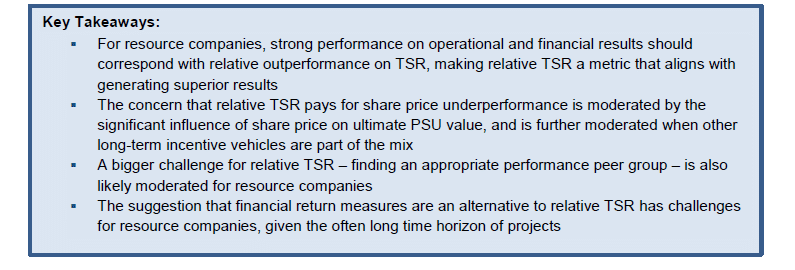

Relative total shareholder return (relative TSR), the most commonly used performance share unit (PSU) measure, has recently been challenged by institutional investors. Earlier this year Ontario Teachers’ Pension Plan (OTPP) released an article entitled “Is Management Compensation Rewarding the Right Behavior?”, which focuses on incentive design in the oil and gas industry. OTPP criticized relative TSR for rewarding management “even when shareholders don’t earn a positive return”.

This alert considers the rationale for using a relative TSR measure for resource companies and provides our perspective on the value of relative TSR as part of a well-balanced long-term incentive design.

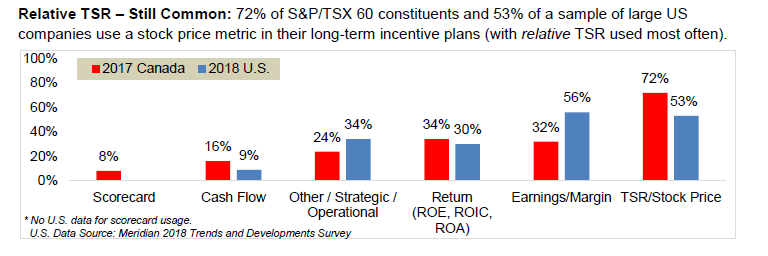

The greater emphasis on relative TSR in Canada is likely due to our high proportion of mining and oil and gas companies, and the particular benefits of relative TSR for resource based companies that are particularly exposed to commodity prices.

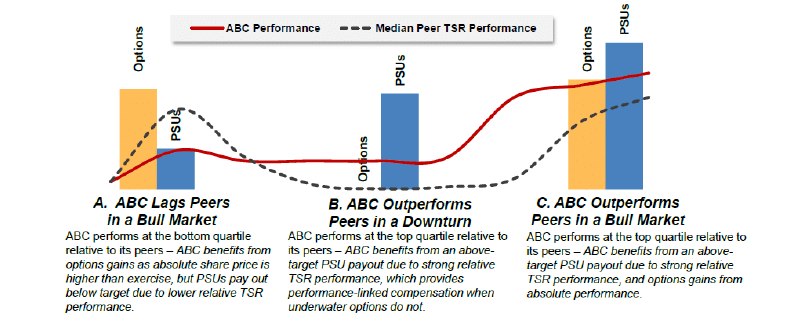

Relative TSR Rewards Industry Outperformance: Relative TSR is designed to reward (or penalize) industry out- or underperformance. For resource companies this is critical, because commodity price movements have a significant impact on share prices at such companies – more so than for other industry sectors where operational performance is relatively more important. Moderating the effect of share price movement on executive compensation allows a resource company to reward operational excellence. This is illustrated in the graphic below, which compares the value of relative TSR performance share units (PSUs) with stock options under various market conditions.

Relative TSR PSUs can:

1. Reward company outperformance in a market downturn, by providing for a higher-than-target multiplier

2. Mitigate the effect of a “rising tide floats all boats” in an up market, by making below-target award payouts for industry underperformance

3. Provide additional upside leverage for outperformance in an up market, through the combination of the above target multiplier and a higher absolute share price

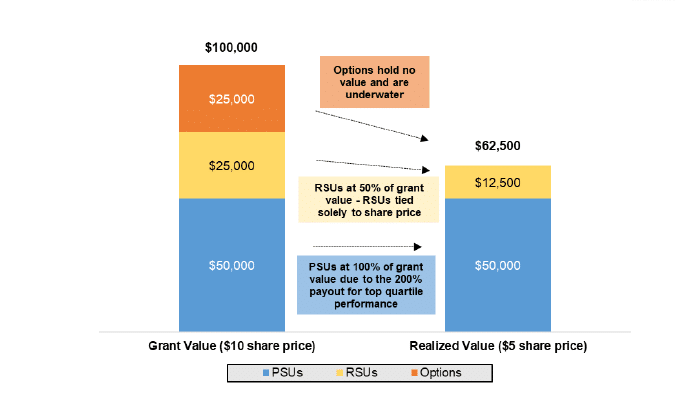

Relative TSR Aligns with the Shareholder Experience: Investors in the resource sector are typically looking for (and prepared to tolerate) share price movement based on commodity price movements, but they generally want to be invested in the best performers in the particular commodity price. Relative TSR PSUs are twice-aligned with shareholders: 1) they reward company outperformance relative to a basket of business peers, using TSR as a proxy for financial and operational outperformance; and 2) the underlying PSU “currency” is company shares (i.e., PSUs are “double-leveraged”). This alignment is even clearer when the whole long-term incentive plan is considered. Consider the graphic below, which compares the grant date value of a $100,000 equity grant with the ending realized value using the following assumptions:

- A typical mix of 50% PSUs, 25% options and 25% restricted share units (RSUs)

- Share price $10 at the start of the period and a $5 share price at the end of the period

- Top quartile relative TSR resulting in a payout factor of 200%

PSUs provide retention and performance-focused value to executives for relative outperformance, even when the industry is in a downturn.

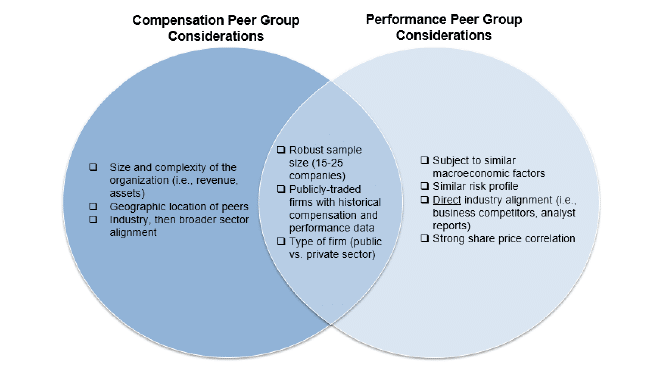

Performance Peer Group: Resource companies (particularly energy companies and certain mining sector companies) have a distinct advantage in performance peer group development (used for relative TSR performance assessment). As resource company performance correlates strongly with commodity price movements (i.e., oil price, gold price), it is typically easier to find companies subject to similar macroeconomic factors when developing a peer group. A robust peer group (i.e., a range of 15-25 companies) minimizes the volatility of performance and pay-related outcomes year-over-year.

Replacing Relative TSR with Financial Return Metrics: OTPP recommends including a financial return measure (e.g., return on capital) in PSUs. We generally support the use of return measures, as they align well with long-term shareholder interests. However, we note that resource companies, in particular, should consider the investment horizons of long-term capital projects, and any potential timing mismatches with the usual three-year time horizon of PSUs. These challenges can be managed through appropriate target setting and also by including a return metric as one of several components of a long-term pay program (in addition, but likely not to the exclusion of a metric like relative TSR).

Absolute TSR Cap: We are seeing more “caps” in relative TSR plans, typically capping the payout at “target” (no upside opportunity) if absolute TSR is negative, regardless of relative outperformance. These caps are supported by institutional investors and make sense in many industries. However, for resource companies an absolute TSR cap may not be the best solution. Adding a cap should be carefully considered, taking into account the effect of lower share price on overall value of long-term incentives, the uncontrollable nature of commodity price movement and the benefits of rewarding high performing management teams in a low commodity price environment.

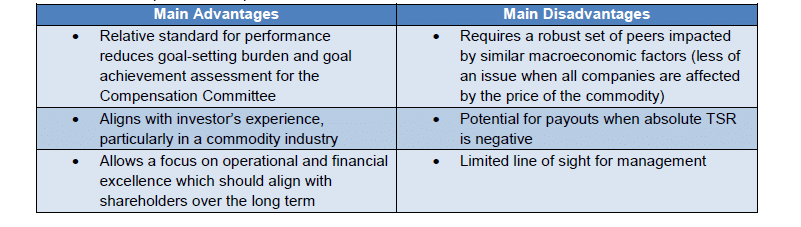

The Bottom Line: For resource companies, we think the advantages outweigh the disadvantages of using relative TSR in a performance plan.

In the End, Resist Homogenization: Relative TSR, particularly as part of a well-balanced long-term plan, achieves a fundamental goal—it rewards management of high performing companies in up and down commodity cycles. As investors in resource companies typically want exposure to commodity price, some reward for high performing companies in the low commodity price cycles is reasonable.

* * * * *

The Client Update is prepared by Meridian Compensation Partners. Questions regarding this Client Update or executive compensation technical issues may be directed to:

Christina Medland at (416) 646-0195, or cmedland@meridiancp.com

Andrew McElheran at (416) 646-5307, or amcelheran@meridiancp.com

Andrew Stancel at (647) 478-3052, or astancel@meridiancp.com

Andrew Conradi at (416) 646-5308, or aconradi@meridiancp.com

Matt Seto at (416) 646-5310, or mseto@meridiancp.com

John Anderson at (847) 235-3601, or janderson@meridiancp.com

This report is a publication of Meridian Compensation Partners Inc. It provides general information for reference purposes only and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com