According to the Meridian 2017 Governance and Incentive Design Survey1, 43% of Meridian 200 companies use an individual performance component in their executive annual incentive plan, typically as a supplement to financial measures. Actual usage may be higher as the 43% does not account for Compensation Committees using discretion to adjust awards for individual performance.

When evaluating whether including an individual performance component is appropriate, companies may want to consider the following questions:

■ Does the company’s culture support differentiating executive payouts based on individual performance or is it more of a team-based approach?

■ Is it appropriate to focus and reward executives for individual performance that may not directly align with financial performance?

■ Might individual performance modifiers help mitigate extremely high or low short-term incentive outcomes?

■ Is the company comfortable disclosing individual goals and achievements, or failure to achieve them, within the Compensation Discussion and Analysis section of the proxy?

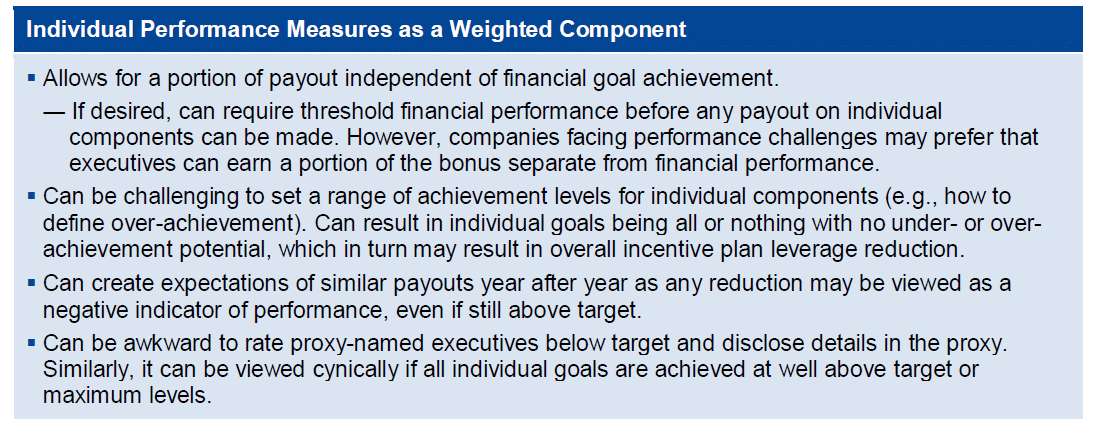

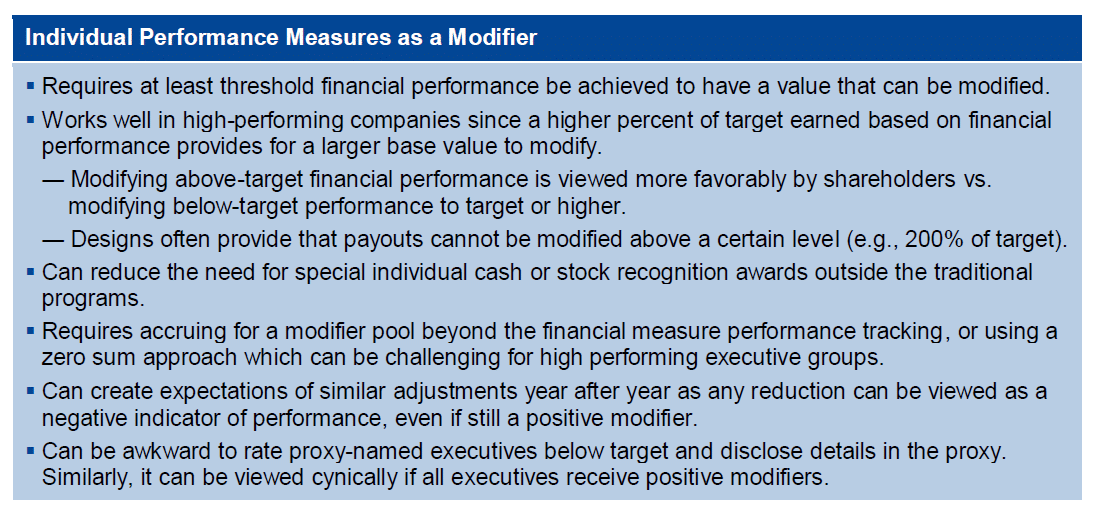

Design Alternatives

There are generally two ways companies use individual performance measures. More than half (58%) of Meridian 200 companies use an individual component as a separately weighted measure, generally 10% to 30% of the overall plan weighting. The other 42% use individual performance as a modifier to the financial results, generally ranging from +/- 15% to 30% of the financial performance results.

Each design has its own advantages and challenges.

The best fit for a particular company will be based on business circumstances, company history, performance expectations and the executive team. The key is to consider how the advantages and disadvantages of each design fit into each company’s culture, compensation philosophy and program objectives.

1 https://meridiancp.com/2017-meridian-corporate-governance-incentive-design-survey/