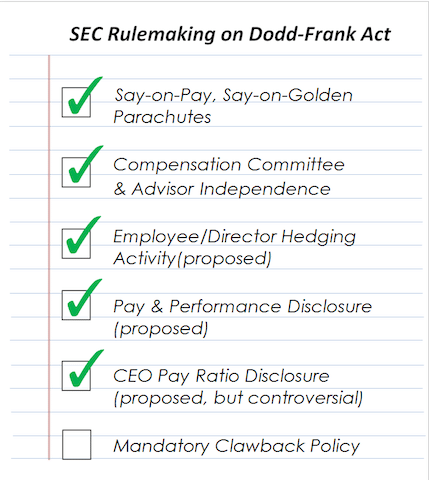

Although the Dodd-Frank Act rules do not apply to most Canadian companies, we watch the slow progress of the regulations with interest as many Canadian companies follow these executive compensation rules as a matter of good compensation governance. Over the past several years, the SEC has issued final rules for say on pay, say on golden parachutes, and the independence of compensation committees and their advisors.

So far this year, progress has been made on rulemaking in two fronts: anti-hedging policies and pay and performance disclosures. No progress has been made on the (seemingly simple) clawback rules or the highly controversial CEO pay ratio proposed rules.

Hedging Activity

In February, the SEC issued proposed rules requiring companies to disclose in their proxy statement whether any employee or board member can engage in “Hedging Transactions” for “Covered Shares”.

- Covered Shares are shares granted as compensation or shares held (directly or indirectly)

- Hedging Transactions are the purchase of financial instruments (including prepaid variable forward contracts, equity swaps, collars and exchange funds) that are designed to hedge or offset any decrease in the market value of company equity securities

Canadian companies are already required under securities law to disclose whether or not Named Executive Officers are prohibited from hedging shares and share based compensation. As a matter of practice, many Canadian companies extended the hedging prohibition to all insiders. The U.S. rules go further, and apply to all employees.

Pay & Performance Disclosure

In late April, the SEC issued proposed rules for a new, standardized approach for pay and performance disclosure, subject to a comment period. The rules require disclosure in the CD&A of the relationship between executive compensation “actually paid” and stock price and dividend performance.

Under the proposed rules, companies disclose the relationship between executive pay and performance, using the company’s total shareholder return relative to the TSR of a peer group or index chosen by the company. The disclosure will be phased in and initially will be for the last 3 years, increasing to the last 5. Separate reporting is required for the CEO and (an average) for the other NEOs.

The proposed rule indicates that compensation “actually paid” be:

Total Compensation as reported in the Summary Compensation Table (SCT)

less

Changes in Pension Value and Value of Stock Awards and Options as reported in the SCT

plus

“Fair Value” of Stock Awards and Options that vested during the fiscal year

plus

Annual Accrual of Pension Benefits during the fiscal year

In effect, compensation “actually paid” in these rule is similar to “realizable pay”.

Clawback Rules

The SEC has yet to issue the proposed rules for the required “clawback” policy. The SEC has not met numerous “self-imposed” deadlines for the release of the regulations under Dodd-Frank. The latest statement by the SEC is that it intends to release clawback regulations by October, 2015, although we have no certainty that this will be the case.

Many Canadian companies have been waiting for the SEC to issue proposed rules. However, an increasing number of Canadian companies have given up waiting and have introduced a clawback to help manage compensation risk and to meet ISS, Glass Lewis and shareholder expectations.

Currently, of the Canadian companies that have voluntarily adopted a clawback, roughly two-thirds have a “triple trigger” clawback requiring:

- A restatement of financials

- Caused by the misconduct of an individual

- Resulting in that individual receiving a higher incentive award than he or she would have under the restated financials

The balance of companies have “double trigger” clawbacks requiring a restatement of financials and a higher incentive award than would have been made under restated financials (misconduct not a requirement).

Meridian Comment. We expect that Canadian practice around clawbacks will move into line with the Dodd-Frank rules in a fairly short period after the eventual release of the rules. While we don’t know what the regulations will provide, the Dodd-Frank legislation mandates that the clawback policy:

- Apply to all current and former executive officers

- Be triggered by an accounting restatement

- Apply to erroneously awarded incentive-based compensation (including stock options) in excess of the amount that would have been paid under the accounting restatement during a 3-year look-back period from date issuer is required to prepare an accounting restatement

This better aligns with the double trigger clawback. Canadian companies that have a triple trigger clawback should wait for the Dodd-Frank rules before revising their policies. Those that don’t have a clawback should consider introducing a triple trigger clawback for next proxy season, if the Dodd-Frank rules are not released this fall.

CEO: Employee Pay Ratio

The SEC issued proposed CEO pay ratio disclosure rules in September 2013. These remain highly controversial and both sides of the debate continue to submit letters to the SEC. If the SEC adopts a final rule in 2015, then the initial CEO pay ratio disclosure may occur in 2016 proxies for the majority of public companies.

Recent legislation has been introduced in the House to repeal the CEO pay ratio disclosure and although passage in the House and Senate is possible, the White House is almost certain to veto any such bill.

* * * * *

The Client Update is prepared by Meridian Compensation Partners. Questions regarding this Client Update or executive compensation technical issues may be directed to:

Christina Medland at (416) 646-0195, or cmedland@meridiancp.com

Andrew McElheran at (416) 646-5307, or amcelheran@meridiancp.com

Andrew Stancel at (647) 478-3052, or astancel@meridiancp.com

Andrew Conradi at (416) 646-5308, or aconradi@meridiancp.com

John Anderson at (847) 235-3601, or janderson@meridiancp.com

This report is a publication of Meridian Compensation Partners Inc. It provides general information for reference purposes only and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.