Jim Heim

Jim Heim

The Say-on-Pay (“SOP”) era has fostered remarkable homogenization in executive compensation program design. The two primary contributing factors are:

1. Expanded compensation disclosure requirements for publicly traded companies, increasing the transparency of competitors’ programs.

2. The heightened influence of proxy advisory firms (“PAF’s”) such as ISS and Glass Lewis with respect to SOP votes; the voting guidelines of both firms are regularly disseminated and discussed in Compensation Committee meetings.

Consequent to the above, it is easier than ever to ascertain what constitutes an outlier program, and there can be real consequences when an outlier program design is coupled with a perceived pay-for-performance (“PFP”) misalignment:

• In situations where an outlier design appears to be overpaying, PAF’s are likely to recommend “against” SOP votes, placing companies in a penalty box where scrutiny of pay programs going forward is heightened and Committee members may be at risk of withhold votes.

• If the outlier design appears to be underpaying, bear in mind that executives have a better sense than past generations of what is typical (due to greater transparency of compensation programs). Such a misalignment may not immediately lead to challenges attracting and retaining talent, but it does create an untenable situation. It is no small thing to ask an executive for complete dedication when they know their pay model is not competitive.

With this as context, companies and sectors that appear to go against the grain in their pay program design merit attention. Pre-commercial biotechnology companies are an excellent example. There are lessons to be learned with respect to how this sector has implemented pay practices that differ from the broader market and the preferred model of PAF’s.

In this four-part series, we examine the current state of pre-commercial biotech CEO pay, how it is tailored to the sector, and what drives differences between companies. We will explore:

Part One: Tailoring Pay to the Business

Part Two: Founders vs. Non-Founders

Part Three: East Coast vs. West Coast

Part Four: Drivers of SOP Results

The Business Model Informs CEO Pay Program Design

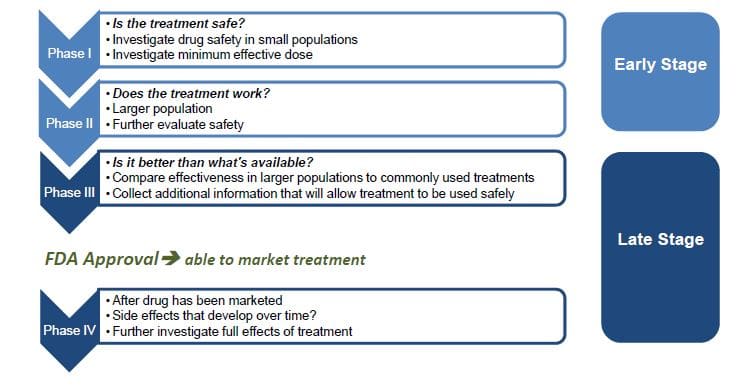

In simple terms, biotech companies progress through three stages:

1. Drug Discovery

2. Clinical Trials focused on gaining Federal Drug Administration (“FDA”) approval

3. Bringing FDA-approved treatments to market through Commercialization

Clinical trials proceed in a series of steps, or phases:

Treatments are typically in Phase I-III for a matter of years or even decades, and companies encounter a high degree of uncertainty with respect to whether a treatment will or will not advance to the next Phase. During this period, pre-commercial companies will most often rely on external financing to generate cash and fund what may be extremely expensive undertakings.

Investors closely monitor pipeline progress and company market value will quickly rise and fall depending on clinical trial success or failure. Valuation of a single treatment may triple upon progress to Phase 2, and triple again upon progress to Phase 3.

Consequently, the sector is characterized by:

• Very long investment horizon between drug discovery and potential commercialization;

• A great deal of uncertainty relating to likelihood and timing of progress through clinical trials;

• Need for significant cash generation from external financing until commercialization;

• Concentration of talent in hot spots in urban areas near feeder universities, research hospitals and venture capital, driving high cost-of-labor;

• Investor focus on pipeline progress more than income statement performance, and

• Volatile stock prices.

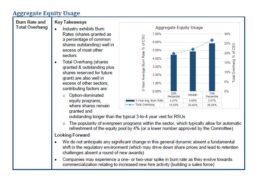

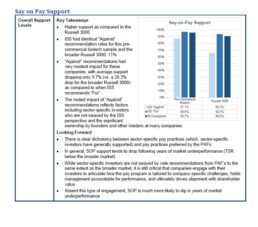

CEO Pay Program Design: Key Takeaways

Our research determined that pre-commercial biotech companies vary from broader market (e.g., Russell 3000) and PAF preferred practices as follows:

Once biotech companies transition to commercialization, the investor focus increasingly shifts to financial results, incentive plans follow suit and there is a clear evolution in pay practices to more closely approximate the pay model in other industries.

![]()

Developing a Roster of Pre-Commercial Biotech Benchmark Companies

In order to investigate CEO pay practices, we isolated publicly-traded biotech sector companies that:

• Were NYSE or Nasdaq listed;

• Were pre-commercial;

• Had annual meetings that included a SOP vote in the 12 month period ending June 1, 2020; and

• Had no CEO turnover in this period.

Ultimately, we identified 18 companies (listed in the Appendix) with key statistics including:

In the remainder of this report, we provide further detail relating to general pay practices, bonus/short-term incentive and long-term incentive design for CEOs, aggregate equity usage statistics and SOP support for the benchmark companies.

Appendix: Companies Included in Study

ADMA Biologics, Inc.

Adverum Biotechnologies, Inc.

Albireo Pharma, Inc.

AnaptysBio, Inc.

Ardelyx, Inc.

Cellular Biomedicine Group, Inc.

CEL-SCI Corporation Concert Pharmaceuticals, Inc.

Corbus Pharmaceuticals Holdings, Inc.

Denali Therapeutics Inc.

Dicerna Pharmaceuticals, Inc.

Editas Medicine, Inc.

Fate Therapeutics, Inc.

GlycoMimetics, Inc.

Mirati Therapeutics, Inc.

Pfenex Inc.

Pieris Pharmaceuticals, Inc.

REGENXBIO Inc.