In our last two postings, we highlighted a number of potential compensation implications for oil & gas companies in the current environment. Beginning with this update, we’ll select some key topics to review in a bit more depth. And, since companies’ annual shareholder meetings are right around the corner, we thought we’d start by highlighting some potential issues and considerations for outside director compensation.

Already we’ve seen energy companies announce dramatic actions to lower capital spend, slash dividends, and reduce G&A expenses. As part of these announcements, some companies have also announced reductions in people-related costs, such as layoffs, some furloughs, and even pay reductions for management and employees.

But what about outside director compensation?

While not a frequent target for companies’ cost-cutting measures, so far we’ve tracked nearly a dozen examples of North American oil & gas industry companies (across all industry segments) that have announced reductions in outside director compensation during this crisis. Nearly all of these appear to be in alignment with announced reductions in named executive compensation. We also forecast that companies will take one of several actions around upcoming equity awards made at the annual meeting. Below we’ve highlighted some potential considerations for thinking about both the cash and equity components of director compensation in the current environment.

Cash Compensation – To Cut or Not to Cut?

In the limited examples we’ve seen thus far, the reductions in outside director compensation have largely been focused on the annual cash retainer. If your company is looking at significant layoffs or widespread employee pay cuts, it may be appropriate to consider some reduction in outside directors’ cash compensation, at least temporarily. For example, if the CEO is taking a 20% salary cut, perhaps outside directors should likewise take a similar haircut.

Additionally, if the Board was scheduled to receive an already approved increase, the Board may wish to consider rescinding that increase.

For cash-constrained companies, we may see the use of equity in lieu of cash; however, cash- constrained companies are likely to face similar pressures on share availability.

Let’s face it, cutting outside director cash compensation is not about achieving aggressive G&A reduction goals. It’s more about showing unity with pay cuts taken by management and employees, especially when there are extensive furloughs, layoffs and other belt-tightening measures being implemented across the organization.

Equity Compensation – How to Size Awards at Low Stock Prices?

Now we get to the million dollar question (actually, it’s more like the $150,000 to $250,000 question):

How do we size equity awards to outside directors (which are typically dollar-denominated) at a time when the stock price has dropped 50% or more since the company made equity grants to management earlier in the year?

Since the majority of oil & gas companies approve grants of new equity awards to outside directors at the annual shareholder meeting, we imagine this question is becoming increasingly common.

Obviously each company’s facts and circumstances are unique, but companies will likely need to review the grant methodology for upcoming awards, taking into account:

■ Share availability,

■ Share dilution,

■ Stock price performance,

■ Approach and stock price used to approve equity grants to management,

■ Actions taken with respect to business operations, and

■ Other company-specific facts and circumstances.

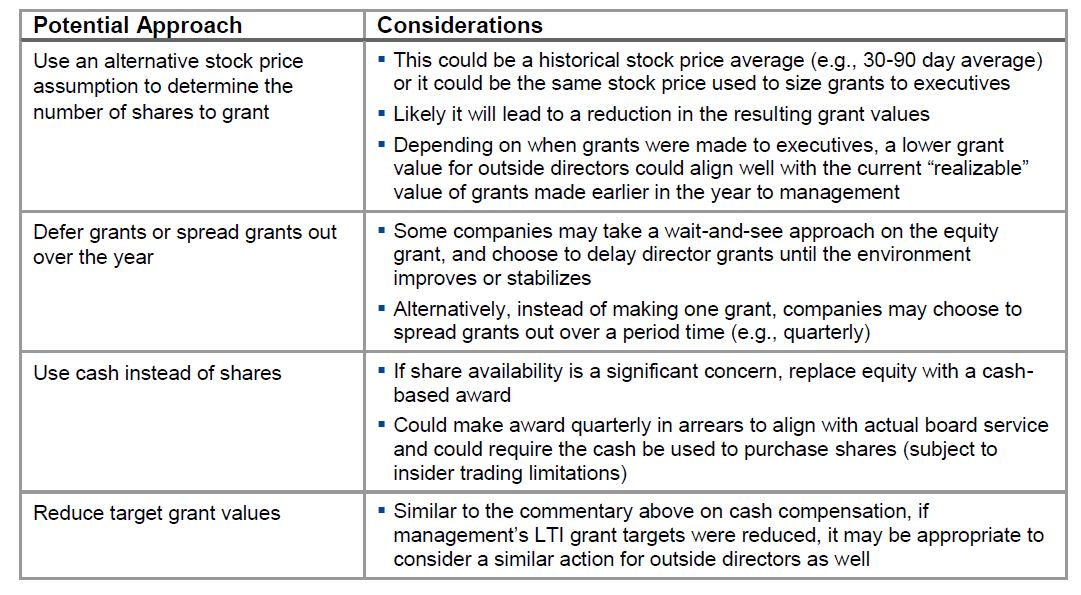

Given the current situation, it is likely that we will see one or more of the following approaches:

While we are likely to have a preview on where things land for 2020 relatively soon, it will be months or perhaps years before we learn whether lower compensation levels – for management and board members alike – become the “new normal.”

If you are interested in reading more about director compensation during times of crisis, then check out this article by our colleague, Jim Heim.