Christina Medland

Christina Medland

Rachael Lee

Rachael Lee

Krunal Billimoria

Krunal Billimoria

Introduction

As companies prepare their proxy disclosures, ensuring transparency and clarity in executive compensation reporting remains a top priority. Investors expect well-structured disclosures that provide insight into board decisions, pay-for-performance alignment, and responsiveness to shareholder concerns.

This update highlights three key areas in proxy disclosure with sample disclosure guidance on why this disclosure may be helpful to include:

1. A letter from the Chair of the Human Resources/Compensation Committee (HRC)

2. Realizable pay: Enhancing pay-for-performance transparency

3. Shareholder engagement following a below 80% say-on-pay vote

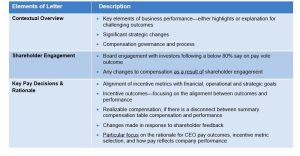

1. Letter from the Chair of the HRC

Why Include a Letter?

A well-crafted letter from the Chair of the HRC sets the stage for the executive compensation discussion. It provides an opportunity to:

• Establish a narrative around compensation philosophy and key decisions, including performance highlights, incentive outcomes, and the link between them

• Address shareholder concerns, particularly after a say-on-pay challenge

• Reinforce the company’s commitment to pay-for-performance alignment

What Should the Letter Contain?

2. Disclosing Realizable Pay: Enhancing Pay-for-Performance Transparency

Why Include Realizable Pay?

Realizable pay disclosure is a powerful way to demonstrate the actual compensation executives have earned and could receive from previously granted awards versus their pay opportunity, typically over a specified performance period. The proxy advisors focus on Summary Compensation Table pay in their quantitative pay-for-performance tests, which does not account for the change in value of equity awards over time. Providing voluntary realizable pay disclosure helps address concerns about perceived pay-for-performance misalignment and enhances transparency for investors and proxy advisors, who regularly reference realizable pay disclosure in their qualitative assessments of the alignment of pay and performance.

Realizable compensation generally includes actual salary paid, the annual incentive paid and the value of equity awards, which reflect changes in share price since the grant date (e.g., the “in the money” value of stock options and the value of RSUs and PSUs using current share price). As the value of equity awards moves in close alignment with share price, realizable pay typically shows much better alignment with shareholder experience than summary compensation table values, particularly if share price has declined.

Approaches to Disclosing Realizable Pay

There are two main approaches for disclosing realizable pay that companies use in their proxy disclosures:

1. Pay-for-Performance Charts: Comparing realizable pay and company performance over time

2. Grant Date Value vs Realizable Value Comparison: Compares the compensation value granted to the executive (either target value or summary compensation table value) with the value of compensation reflecting performance and share price outcomes

Examples from of Disclosure:

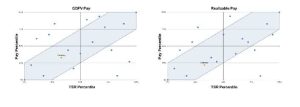

1. Pay-for-Performance Chart

• Compares CEO realizable pay rank vs. TSR pay rank over three years

• Also provides comparison of CEO grant date fair value pay rank vs TSR pay rank over three years

• The scatterplot charts provide clear percentile-based comparison against peers with the shaded region supporting the message that CEO pay aligns with performance relative to the market

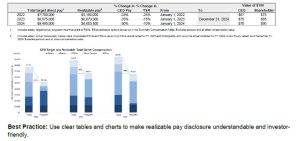

2. Comparison of Grant Date Value vs Realizable Value

• Provide a detailed breakdown of realizable pay by compensation component

• For example, the table compares target direct pay vs. realizable pay over three years, showing how realizable compensation outcomes have been lower than the target due to share price performance

• The bar chart clearly shows how realizable compensation compares to target compensation across different pay elements (salary, bonus, stock options, RSUs, PSUs)

• Matches the periods of realizable pay valuations to the periods of TSR, which demonstrates a direct link between pay and performance

• Includes a clear methodology for how realizable pay is calculated, enhancing investor understanding

3. Disclosing Shareholder Engagement After a Low or Failed Say-on-Pay Vote

Why Include Information on Shareholder Engagement?

If a company receives low shareholder support (<80%) for say-on-pay, proxy advisors and institutional investors expect clear disclosure of how the board responded. The best disclosures outline notable engagement efforts:

• Number (or percentage) of investors the company requested to meet

• Number of investors met with and their total percent of shares owned

• Key feedback received and steps taken to conduct an independent review of the compensation program

• What changes to compensation or governance were made to address investor concerns

• Any ongoing governance enhancements or planned changes to compensation programs

• Any ongoing engagement strategy to maintain a dialogue with shareholders beyond proxy season

Best Practice: Where possible, quantify engagement efforts (e.g., % of share/investors represented, number of meetings) and provide specific details on program changes to demonstrate responsiveness in the disclosure. It may also be helpful to formally communicate changes prior to proxy disclosure, and, depending on the seriousness of investor concerns, to have a second engagement with shareholders, ahead of the publication of the following year’s proxy to discuss changes made and ensure investors have clarity well in advance of the next say-on-pay vote.

Final Thoughts

Transparent proxy disclosure is essential for building investor trust, particularly in today’s evolving corporate governance landscape. Companies should proactively refine their proxy statements to effectively communicate pay-for-performance alignment, shareholder responsiveness, and governance best practices.

By leveraging these best practices and the above examples, issuers can strengthen their proxy disclosures and enhance shareholder confidence.

* * * * *

This Client Update is prepared by Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

Questions regarding this Client Update or executive compensation technical issues may be directed to:

Christina Medland at (416) 566-1919 or cmedland@meridiancp.com

Andrew McElheran at (647) 472-7955 or amcelheran@meridiancp.com

Matt Seto at (647) 472-0795 or mseto@meridiancp.com

Andrew Stancel at (647) 382-7684 or astancel@meridiancp.com

Andrew Conradi at (647) 472-5231 or aconradi@meridiancp.com

Rachael Lee at (647) 975-8887 or rlee@meridiancp.com

Kaylie Folias at (416) 891-8951 or kfolias@meridiancp.com

Krunal Billimoria at (647) 267-5869 or kbillimoria@meridiancp.com

Jason Chi at (647) 248-1029 or jchi@meridiancp.com

Wali Ahmed at (647) 208-0132 or wahmed@meridiancp.com

Gabrielle Milette at (905) 242-0503 or gmilette@meridiancp.com

Steve Li at (437)451-2710 or sli@meridiancp.com

Paakavy Senthamilarasan at (647) 926-5641 or psenthamilarasan@meridiancp.com