Ed Hauder

Ed Hauder

Nathan Williams

Nathan Williams

On May 19, 2026, the SEC released proposed rulemaking (Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies (Release No. 33-11419)1), which represents the most significant overhaul of the public company filer-status framework in over two decades. Comments are due on or before July 20, 2026. In summary, public companies with a public float below $2 billion will see significantly reduced disclosure requirements for executive compensation, including the elimination of the Say-on-Pay vote requirement.

Key Changes

• Reduces the five overlapping filer categories into two primary groups: Large Accelerated Filers (LAFs) and Non-Accelerated Filers (NAFs), with a new Small Non-Accelerated Filers (SNFs) sub-category for NAFs.

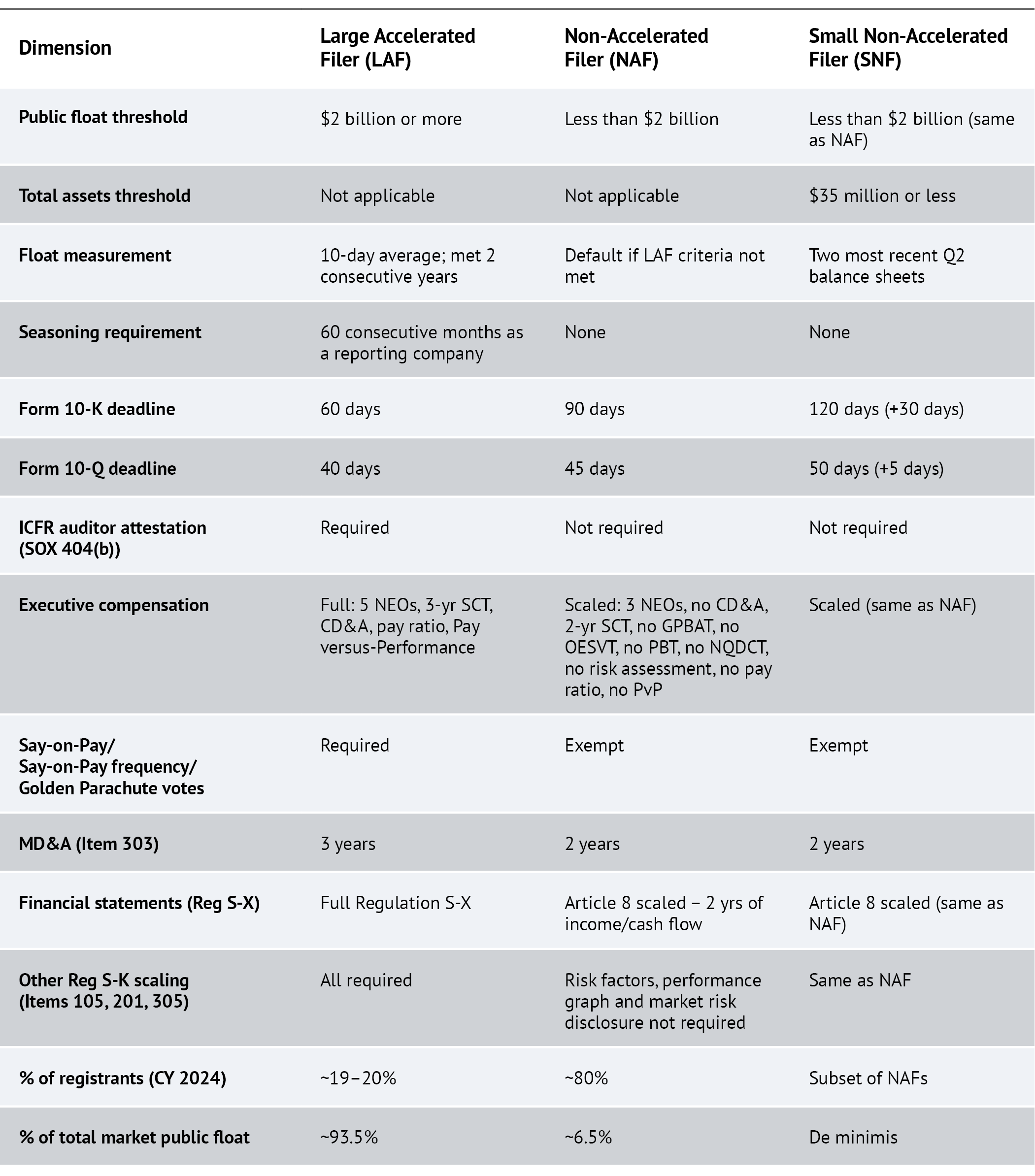

LAF Classification Criteria:

― Raises public-float threshold from $700M to $2B (using the average closing price over the last 10 trading days of Q2 multiplied by the non-affiliate share count at quarter-end; the threshold must be met at two consecutive annual measurement dates).

• Requires a minimum of 60 consecutive months as a reporting company before a newly public company can become an LAF.

― SEC estimates that approximately ~19.2% of registrants would be LAFs under revised designation, versus 35.4% today.

NAF Classification Criteria:

― Less than $2B in public float (as defined above).

― SEC estimates that approximately 80.8% of registrants would be NAFs under revised designation, versus approximately 44% today.

SNF Classification Criteria (Sub-Category of NAF):

― Less than $2B in public float + $35M assets or less.

― Note: Emerging Growth Companies (EGCs) status remains on the books, but the new NAF accommodations would make reliance on EGC status unnecessary in most circumstances.

• Provides extended filing deadlines (for 10-K and 10-Q) and disclosure accommodations to newly classified NAFs and SNFs (similar to those currently available to Smaller Reporting Companies (SRCs)/EGCs) (see detailed list below).

• The SEC estimates that the group of companies qualifying as NAFs (including SNFs) will represent an additional 37% of companies compared to the current number of companies qualifying as SRCs, a significant increase in the number of companies subject to scaled-back disclosure requirements.

Disclosure Implications for NAFs

For companies that will qualify as NAFs, the proposed rule significantly curtails executive compensation requirements for proxy statements and other disclosures:

• No Say-on-Pay, Say-on-Pay frequency or Say-on-Golden Parachutes votes

• Reduced number of Named Executive Officers (NEOs) (from 5 to 3)

• Only two (2) years covered in the Summary Compensation Table (SCT)

• No Compensation Discussion & Analysis (CD&A) section

• No supplemental compensation tables, including Grants of Plan-Based Awards Table (GPBAT), Option Exercises and Stock Vested Table (OESVT), Pension Benefits Table (PBT), • Nonqualified Deferred Compensation Table (NQDCT)

• No CEO pay ratio disclosure

• No Pay versus Performance disclosure

• No compensation committee report

• No compensation committee interlocks and insider participation

• No auditor ICFR attestation requirement

For broader financial filings, NAFs would only be required to report on 2 years for both financial statements and Management Discussion & Analysis reporting, and would no longer be required to provide risk factors, a performance graph, or market risk disclosure.

The following chart compares the two filer categories and the one new filer subcategory to illustrate the key differences, including disclosure requirements and filing deadlines.

By redefining the filer status and extending the accommodations provided to SRCs and EGCs to NAFs, the SEC has effectively reduced the disclosure and filing burden for many companies and reduced the number of companies subject to certain Dodd-Frank requirements (i.e., Say-on-Pay vote, Say-When-on-Pay votes, Say-on-Golden Parachute votes, CEO pay ratio, and Pay versus Performance), which it could not otherwise eliminate unless Congress also acted.

Proposed Filer-Status Framework: LAF vs. NAF vs. SNF

Key Takeaway: LAF status compresses to top ~20% of registrants (~93.5% of public float); all others become NAFs with scaled disclosure, and the smallest (≤$35M assets) get extra filing time as SNFs.

Meridian Perspective

The SEC will accept comments on the proposal through July 20, 2026. The proposal is consistent with the SEC Chair’s broader focus on simplification and reducing compliance costs and reporting burdens for smaller public companies. While we expect some pushback from institutional investors and governance groups that have been critical of the SEC’s scaled-back disclosure agenda, we anticipate the SEC will adopt the rule substantially as proposed, with only minor modifications, if any. Consequently, it is possible these rules could be effective for the 2027 proxy season.

For the largest public companies, it will remain business as usual. Smaller and newer public companies, however, should begin evaluating the potential implications of the proposed changes and how the revised requirements could impact their disclosure practices.