On November 24, 2021, the Securities Exchange Commission issued Staff Accounting Bulletin (“SAB”) 120 which, among other items, expresses the views of the SEC staff regarding the estimation of the fair value of share-based payments (e.g., equity incentive grants), when a company is in possession of material non-public information.

SAB 120 would require a company that grants a spring-loaded equity award (i.e., the grant of an equity award in advance of and in connection with the disclosure of material positive non-public information) to determine whether the fair value of the award should be based on a share price that takes into account share price movement due to the disclosure of such information. Prior to SAB 120, accounting standards generally required a company to use the grant date share price to determine the grant date fair value of equity awards. Fortunately, the application of SAB 120 appears narrow and is unlikely to affect the valuation of annual cycle equity grants.

Background

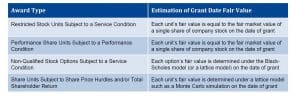

Typically, the estimation of the grant date fair value of a share-based payment is a relatively straightforward undertaking pursuant to the applicable accounting standards (i.e., ASC Topic 718). The table below

illustrates valuation methodologies to determine the grant date fair value of various equity vehicles:

Equity awards with complex structures (e.g., one subject to a performance condition with payout subject to modification (+/- 20%) based on a relative total shareholder return modifier) may

require the use of more complex valuation techniques to estimate the awards’ grant date fair value.

Regardless of valuation technique employed to estimate an equity award’s fair value, all valuation models use a common input – grant date share price. This input forms the bedrock of the various valuation models.

SAB 120 Changes Determination of Fair Value When a Company Grants Equity Awards While in Possession of Material Non-public Information

The SEC staff has modified this bedrock of valuation models; the staff view is that under certain circumstances, a company’s current share price value may not be appropriate to use in determining fair value of a share-based arrangement.

Specifically, SAB 120 provides that current share price may be inappropriate to use when (i) a company grants equity awards in contemplation of, or shortly before, a planned release of positive material non public information and (ii) such information is expected to result in a material increase in share price. In such a circumstance, the staff believes a company should consider whether adjustments to the current share price are appropriate when estimating the fair value of an equity grant. Interestingly, SAB 120 provides no specific guidance as to appropriate methods a company may use to adjust share price.

To illustrate when an adjustment to current share price may be appropriate, SAB 120 includes the following example:

Facts: Company D is a public company that entered into a material contract with a customer after market close. Subsequent to entering into the contract but before the market opens the next trading day, Company D awards stock options to its executives. The stock option award is non-routine, and the award is approved by the Board of Directors in contemplation of the material contract. Company D expects the share price to increase significantly once the announcement of the contract is made the next day. Company D’s accounting policy is to consistently use the closing share price to determine the grant date fair value of equity awards.

SEC Staff Interpretive Response: In estimating the grant date fair value of stock options in this fact pattern, absent an adjustment to the closing share price to reflect the impact of Company D’s new material contract with a customer, the staff believes the closing share price would not be a reasonable and supportable estimate and, without an adjustment, the valuation of the award would not meet the fair value measurement objective of FASB ASC Topic 718 because the closing share price would not reflect a price that is unbiased for marketplace participants at the time of the grant.

Meridian comment. The determination of fair value for annual cycle grants appears not to be affected by SAB 120.

The implications of SAB 120 on equity grant valuations appears to be limited and principally aimed at “spring-loaded” equity awards (i.e., awards granted in advance of and in connection with the disclosure of positive material non-public information). According to the SEC staff, SAB 120 would not apply to routine annual equity grants that are not designed to be “spring-loaded”. This exception to SAB 120 should cover the vast majority of equity grants made by public companies. However, care should be taken with respect to out-of-cycle grants, such as promotion grants, sign-on awards and special grants. Companies should consider the underlying circumstances of such grants and whether the grants are being made in anticipation of, or shortly before, the disclosure of positive material non-public information. Companies should also consider how to document their conclusion in the record. To obtain definitive advice on the application of SAB 120 to a particular equity grant, public companies should obtain opinions from its internal finance function and external auditor (and legal counsel, if appropriate).

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Governance and Regulatory Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com