Jared Berman

Jared Berman

Tina Murphy

Tina Murphy

Companies are increasingly focused on succession planning, leadership continuity, and proactive executive transitions. Yet some compensation programs may unintentionally reward retirement-eligible executives for delaying retirement until the company initiates a separation.

In particular, retirement-eligible executives may find that an involuntary termination without cause produces a more favorable monetary outcome than voluntary retirement. In some cases, executives may also seek to receive cash severance benefits available under employment agreements or severance plans while simultaneously benefiting from the more favorable retirement treatment of equity contained in their equity award agreements.

While rarely intentional, this “double-dipping” or “best of both worlds” outcome can create incentives for executives to remain employed until the company initiates a separation rather than voluntarily retire in support of succession planning objectives.

Meridian has previously written about the importance of thoughtful retirement definitions and post-termination equity treatment design. As SERPs and other supplemental retirement programs have become less prevalent, equity award treatment has increasingly become the primary benefit for many retirement-eligible executives.

This article, though, examines a more specific, and increasingly relevant issue: whether companies are unintentionally creating incentives for retirement-eligible executives to wait for a company-initiated separation rather than voluntarily retire.

To illustrate, consider a retirement-eligible executive whose equity awards would continue vesting upon retirement. If the same executive remains employed until an involuntary termination without cause, they may receive prorated equity treatment plus cash severance equal to one or two times salary and target bonus. In some cases, the executive may seek both cash severance benefits and retirement treatment on equity awards, creating a substantially more favorable outcome than voluntary retirement.

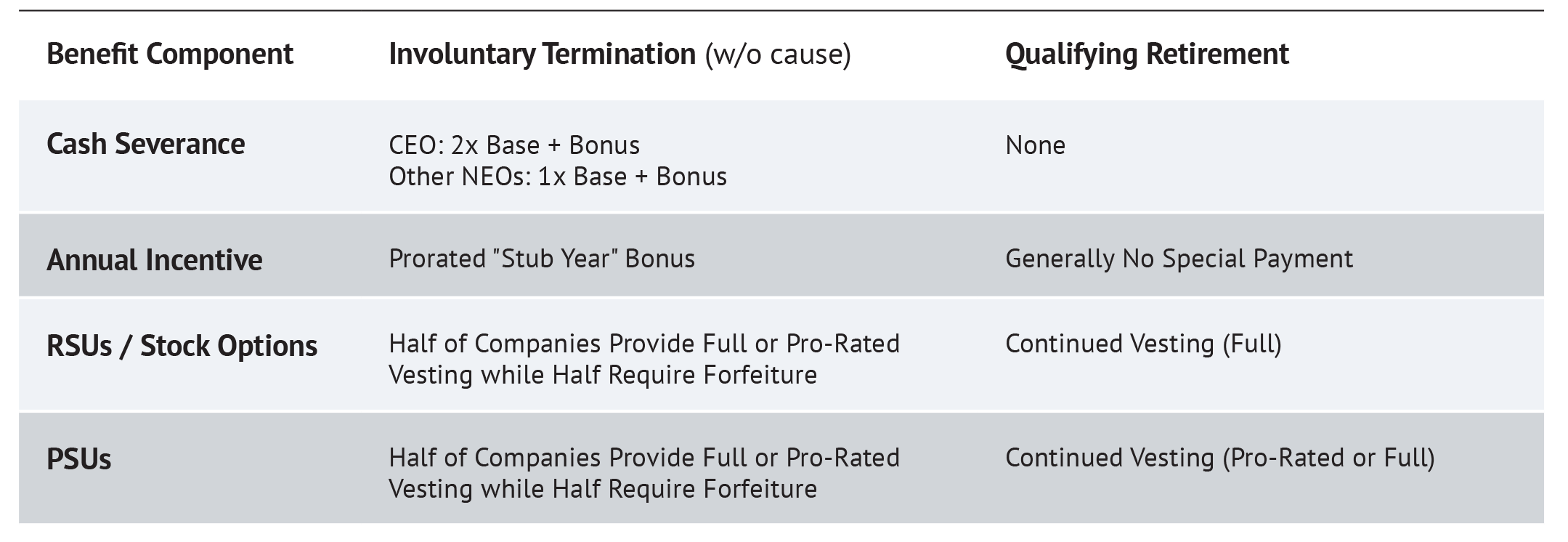

The Disconnect Between Severance and Retirement Treatment

Using common market practices observed in Meridian’s recent severance study and our review of retirement provisions, the following table illustrates how involuntary termination and retirement outcomes often compare.

Viewed independently, both severance and retirement provisions may appear reasonable. The challenge emerges when companies fail to evaluate how these arrangements interact once an executive becomes retirement eligible.

Cash severance protections are typically established through employment agreements, severance plans, or executive severance policies. Retirement treatment, however, is generally governed by equity award agreements or the omnibus plan, which often supersede broader plan provisions with respect to post-termination equity treatment.

As a result, retirement-eligible executives may seek the benefits of both arrangements — receiving cash severance following an involuntary termination while also preserving retirement treatment for their equity awards. In these situations, remaining employed until the company initiates a separation may be financially more attractive than voluntarily retiring.

Why This Matters

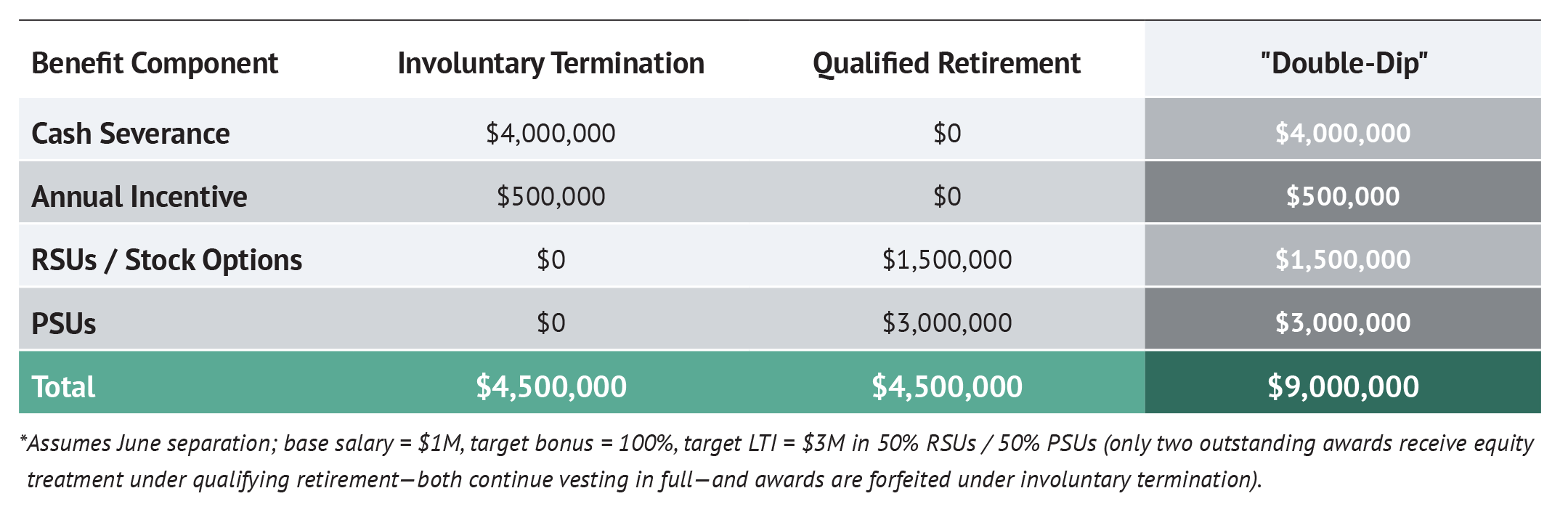

This misalignment creates important governance and succession planning considerations for compensation committees and boards. When retirement-eligible executives can receive cash severance under an involuntary termination arrangement while also benefiting from retirement treatment on their equity awards, the incentive to remain employed until a company-initiated separation can become difficult to ignore (shown below).

Illustrative CEO Benefit Values*

In practice, this can create several challenges:

• Delayed succession timelines

• Increased reliance on involuntary termination processes

• Higher overall separation costs

• Extended transition arrangements, including advisory or consulting roles designed to facilitate continued cash payments and equity vesting

• Tension between organizational planning objectives and executive incentives

Importantly, this imbalance does not necessarily reflect poor program design in isolation. Severance programs and retirement provisions are often developed independently over time, with different objectives in mind.

This challenge often emerges when companies move from policy design to an actual executive transition. Severance and retirement provisions are typically established in the clear light of day, without a specific executive or situation in mind. However, when a respected, long-tenured executive approaches retirement, compensation committees may face pressure to provide a more favorable outcome than contemplated by the original design. Clear policies are therefore critical, as exceptions made for one executive can quickly become precedents that shape expectations for future transitions.

Beyond economics, compensation committees should consider whether separation outcomes are producing behaviors consistent with board objectives. If retirement-eligible executives have a financial incentive to postpone retirement discussions or succession planning conversations, the compensation framework may be working against the leadership transition outcomes it was intended to support.

Evaluating Separation Programs Holistically

As companies review executive compensation arrangements, an increasingly important question is not simply whether severance or retirement provisions are individually reasonable, but whether the overall framework appropriately aligns with organizational objectives.

In some cases, companies may determine that involuntary termination protections remain appropriate given market practice and executive retention considerations. In others, organizations may conclude that the economic gap between involuntary termination and retirement outcomes has become too significant.

Addressing the issue does not necessarily require enhancing retirement benefits or reducing severance protections. Rather, companies should evaluate how employment agreements, severance plans, and equity award agreements interact once an executive becomes retirement eligible.

A key objective should be avoiding unintended “double dipping” outcomes while ensuring that retirement and involuntary termination scenarios produce reasonably aligned economic results. Retirement-eligible executives should generally receive either involuntary termination benefits or retirement treatment, not the most favorable elements of each.

Compensation committees should carefully evaluate whether equity treatment upon an involuntary termination remains appropriate once cash severance is considered. In many cases, the value of severance alone may already produce an outcome that is comparable to — or more favorable than — retirement treatment, meaning that even modest equity vesting provisions can quickly create a significant economic advantage for involuntary termination. Given that these separations often occur in the context of leadership change or performance concerns, some companies may consider prorated vesting (or forfeiture) for unvested time-based awards while requiring forfeiture of unvested PSUs, better aligning separation outcomes with pay-for-performance principles and succession planning objectives.

Questions for Compensation Committees

As boards and compensation committees continue to focus on executive succession and leadership continuity, several questions may warrant consideration:

• Are current arrangements creating incentives to delay retirement?

• Would a retirement-eligible executive be financially better off waiting to be terminated than

voluntarily retiring?

• Could executives receive both cash severance and retirement treatment on equity awards following an involuntary termination under the company’s current plan and award language?

• Is the company relying excessively on ad hoc or discretionary solutions?

• Does the overall framework support the succession planning objectives the company is attempting

to achieve?

Executive separation design is often evaluated through the lens of competitiveness and retention. However, compensation committees should also consider whether their programs support orderly leadership transition. If retirement-eligible executives are financially incentivized to wait for a company-initiated separation rather than voluntarily retire, the compensation framework may be undermining the very succession planning objectives it was designed to support.

Meridian frequently assists companies in modeling and valuing executive separation outcomes under various separation scenarios, helping compensation committees evaluate whether severance and retirement programs are operating holistically and supporting intended retention, succession planning, and governance objectives.