Christina Medland

Christina Medland

Rachael Lee

Rachael Lee

The Issue and the Shift

For more than a decade, North American executive compensation programs have moved to have at least 50% of long-term incentives (LTI) vest based on performance, typically through 3-year performance share units (PSUs). This structure has been reinforced by third-party expectations, including proxy advisor policies. Dominant Canadian market practice is for public companies to allocate at least 50% of LTI to PSUs. However, this trend to homogeneous LTI programs may be coming to an end.

Five factors in the market may be driving a shift towards longer vesting restricted share units (L-RSUs):

1. Some investors are asking whether PSUs are effective to drive better long-term shareholder returns. Critics argue that PSU programs are complex, poorly disclosed, promote short-term thinking and create incentives to manage compensation outcomes, rather than shareholder value creation. Relative total shareholder return (r-TSR) has come under particular scrutiny in the commodity sectors for rewarding the “least worst” performers.

2. Proxy advisors (ISS and Glass Lewis) have indicated some receptivity to treating L-RSUs as equivalent to PSUs. This softening, combined with what appears to be a decline in proxy advisor influence, allows for greater flexibility in LTI vehicle mix based on the business strategy.

3. European investors are increasingly critical of PSUs, particularly PSU target setting (in many cases due to a perception of lack of rigour) and some strongly prefer L-RSUs. As these investors take positions in North American companies, they apply the same concerns to North American compensation programs1, which may shift the position of other institutional investors. Currently, major institutional investors in North America like Blackrock and Vanguard have not changed their position.

4. Macro-economic, geographic and other volatility has put increasing pressure on companies’ ability to set realistic and rigorous long-term performance goals (outside TSR relative performance goals).

5. Sustained periods of volatility (COVID, geopolitical uncertainty and anxiety over AI) may increase the need for long-duration, shareholder aligned and transparent LTI.

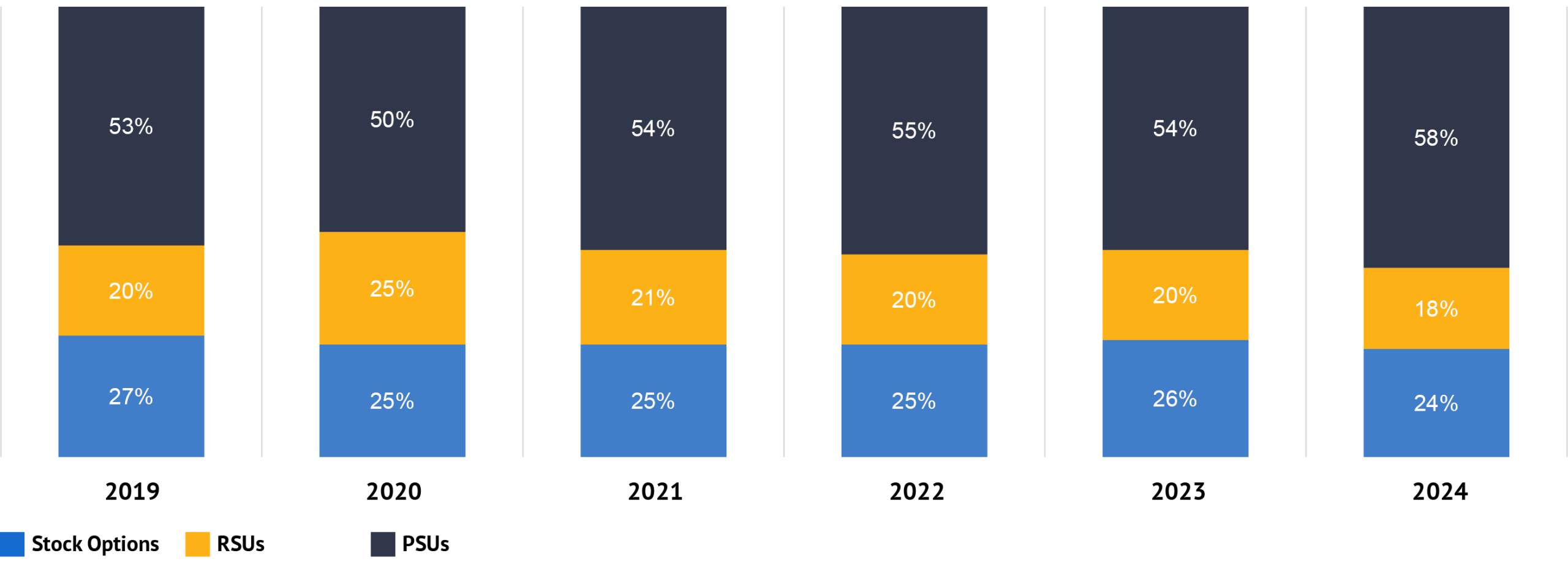

Current Canadian Market

Among TSX 60 companies, the weighting to stock options in LTI plans has remained flat over the last 5 years. The weighting to PSUs has increased, and weighting to RSUs has decreased over the same period.

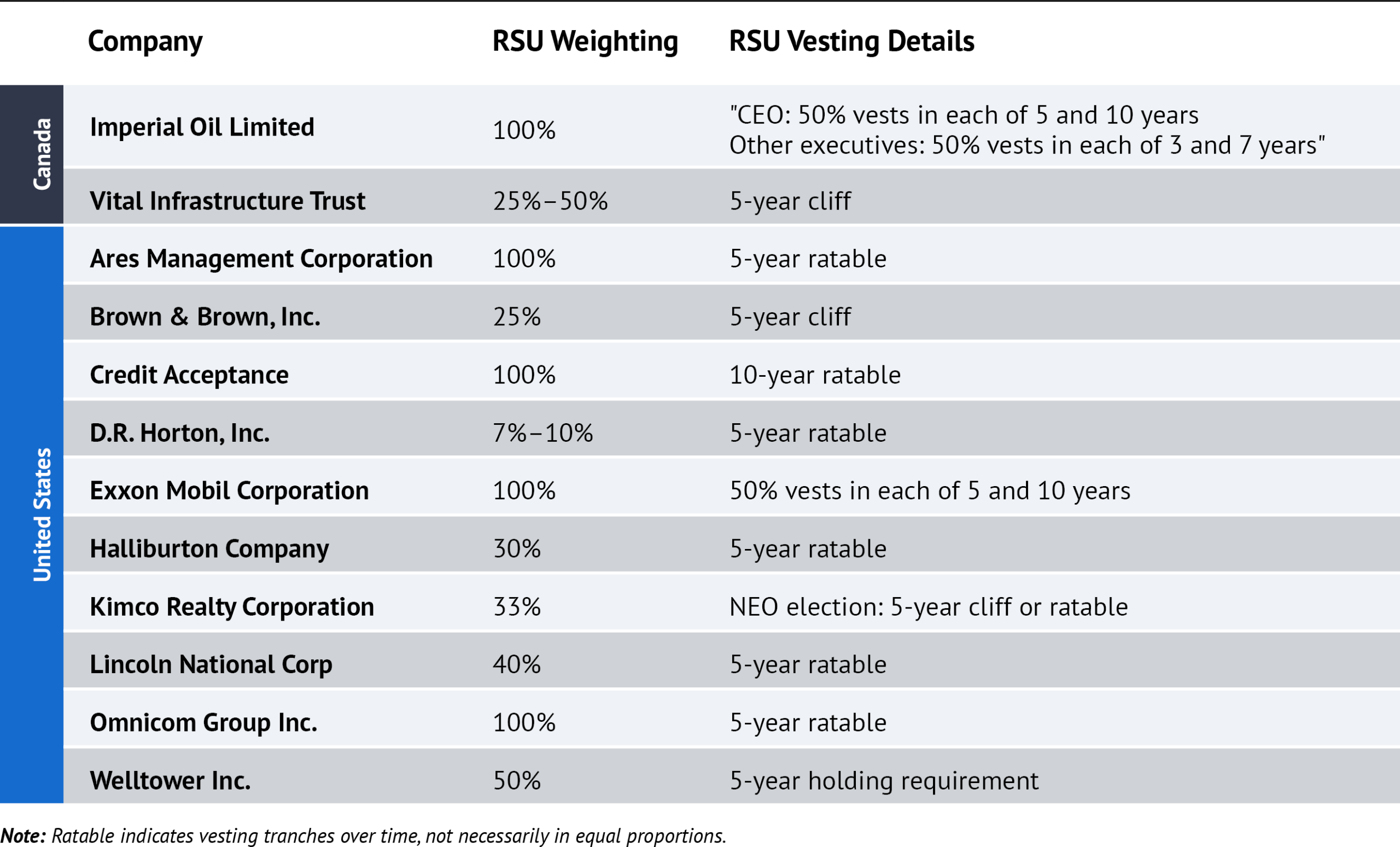

Market Examples of Longer Vesting RSUs:

Broad adoption of long-vesting RSUs in North America is limited, as this is an emerging trend. The following companies provide RSUs with 5-year vesting, or longer.

While adoption remains limited, these examples illustrate that longer-duration equity structures are no longer theoretical. The more relevant question for boards is whether a longer vesting horizon would better support their strategic objectives, talent needs and shareholder expectations than a traditional PSU-heavy design.

Advantages and Disadvantages of Longer-Vesting RSUs

Advantages

There are several advantages of L-RSUs:

• Sustained exposure to share price performance over extended periods should provide stronger alignment with shareholder outcomes and reinforce ownership mindset among executives. Viewed by some investors as a meaningful measure of pay-for-performance.

• Retention in both positive and negative share price performance environments may support leadership continuity during periods of transformation, succession, or market volatility.

• L-RSUs do not require long-term performance targets to be set, eliminating the risk that targets become either unachievable or insufficiently rigorous as business and market conditions evolve over time. This also simplifies the compensation program overall.

Considerations

• For mature or steady-state companies, L-RSUs may become a “breathe and receive” vehicle, with no direct link to performance. Extended vesting alone may not provide the same focus on key strategic and operational objectives as PSUs.

• L-RSUs lack the upside leverage and downside risk of PSUs, creating lower shareholder aligned wealth creation opportunities at high performing companies.

• L-RSUs limit reward to share price performance, which may reflect broader market, sector, or macro-economic factors beyond management’s direct control.

• Without appropriate consideration for termination and good leaver provisions (e.g., pro-rata vesting by default, which may be overridden for “good leavers”), L-RSUs may create unintended consequences related to executive retention.

• First movers may encounter resistance from executives who may in turn expect a “value premium”, particularly in a market where 3-year vesting is still the dominant design – from the recipient’s perspective, longer-dated vesting compared to traditional 3-year vesting is a takeaway.

Achieving Longer-Term Vesting for Canadian Companies

The Canadian Income Tax Act, (ITA), significantly restricts the deferral of compensation through salary deferral arrangement rules (SDA). The three typical avenues for a Canadian company to provide tax deferred compensation are:

The “3-year bonus exception” to the SDA rules

• A majority of Canadian public company equity is awarded under this exemption, which limits the tax deferral to the shorter of the vesting date and ~3 years

• This has resulted in a dominant market practice limiting RSU and PSU vesting and performance periods to 3 years

The “deferred share unit (DSU) exception” to the SDA rules

• This exception allows an indefinite tax deferral, subject to some key restrictions:

– The value delivered must be based on the value of shares of the company

– DSUs cannot be monetized while the executive holds any employment or board role with the company

– DSUs must be monetized by the end of the year following retirement from all roles with the company

• This exception is commonly used to award DSUs to directors, but is also used for executives—commonly on a voluntary basis and frequently limited to the share ownership requirement

– The inability to monetize DSUs during employment is a significant impediment to large scale use of DSUs for executive compensation

A treasury-settled share unit under section 7 of the ITA

• This provision allows for a longer deferral of tax and some flexibility to choose the time to redeem share units—this provides the flexibility for L-RSUs; however:

– Treasury share unit plans are dilutive (like stock option plans), shareholders must approve the treasury reserve for the issuance of shares pursuant to the plan

– These plans cannot provide redemption flexibility for U.S. taxpayers

– These plans are best used for senior executives who are expected to hold vested RSUs for long periods of time

Implications for Long-Term Incentive Design

As the discussion around PSUs and L-RSUs continues to evolve, companies may reassess whether their current weighting to PSUs is most effective approach for supporting long-term shareholder alignment, retention and executive accountability. Management and compensation committees may place greater emphasis on designing LTI programs that reflect their business strategy, talent priorities, industry dynamics and shareholder perspectives.

At the same time, evolving investor and proxy advisor views may provide companies with greater flexibility to incorporate simpler or more ownership-oriented equity structures into executive compensation programs while continuing to maintain strong governance alignment.