The SEC’s adoption of the Final Rule represents the culmination of a years’ long effort to require greater transparency and accountability of PAFs. Specifically, the Final Rule:

■ Conditions the availability of certain existing exemptions from the information and filing requirements of the federal proxy rules for PAFs upon compliance with additional disclosure and procedural requirements.

■ Codifies the SEC’s interpretation that proxy voting advice generally constitutes a solicitation within the meaning of the Securities Exchange Act of 1934 (“Exchange Act”).

■ Amends the proxy rules to clarify when the failure to disclose certain information in proxy voting advice may be considered misleading within the meaning of the rules.

PAFs’ Exemption from Proxy Rules Conditioned on Compliance with Certain Disclosure and Procedural Requirements

Historically, the SEC has exempted certain kinds of solicitations from the proxy rules (i.e., information and filing requirements). For example, the SEC has exempted communications by persons not seeking proxy authority and proxy voting advice given by advisors to their clients under certain circumstances. PAFs have historically relied on these exemptions to provide proxy voting advice, without the necessity of complying with the filing and information requirements of the proxy rules.

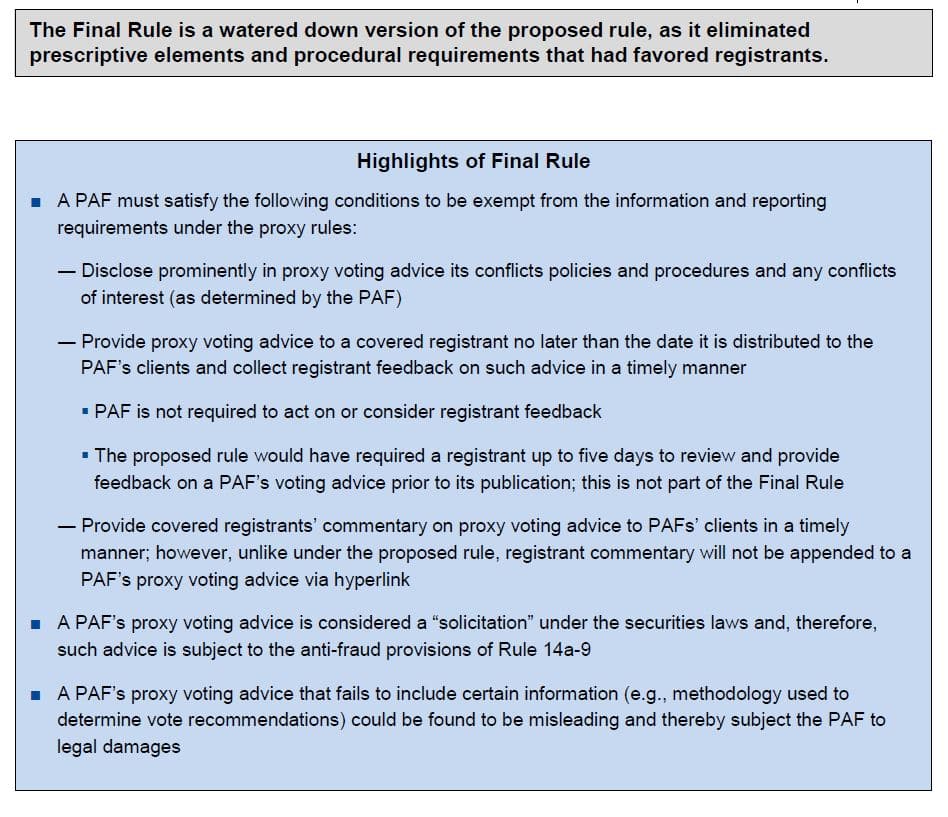

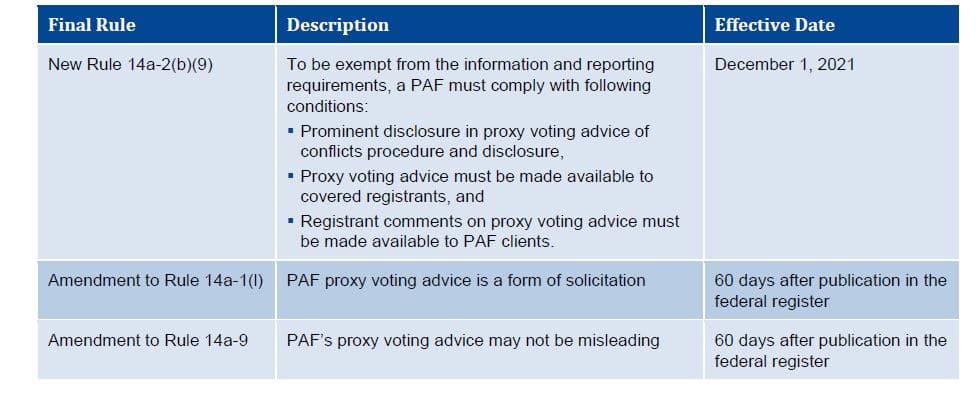

The Final Rule makes these exemptions conditioned upon a PAF’s compliance with the following requirements, which are further described below: (i) disclosure of conflicts procedures, (ii) adoption of written policies and procedures designed to ensure that the PAF’s proxy voting advice is made available to registrants and (iii) adoption of written policies and procedures designed to ensure that the PAF provides clients with a registrant’s views about the proxy voting advice, so that they can take such views into account as they vote proxies (collectively, “Exemption Requirements”).

Disclosure of Conflicts Procedure (“Conflicts Rule”)

General Rule. The Final Rule imposes a conflicts disclosure framework on a PAF who wishes to use the exemption from the information and filing requirements. Under the Final Rule, a PAF must include in its proxy voting advice (or in any electronic medium used to deliver the advice) prominent disclosure of:

■ Any information regarding an interest, transaction, or relationship of the PAF (or its affiliates) that is material to assessing the objectivity of the proxy voting advice in light of the circumstances of the particular interest, transaction, or relationship; and

■ Any policies and procedures used to identify, as well as the steps taken to address, any such material conflicts of interest arising from such interest, transaction, or relationship.

Determination of Conflict by PAF. In the release of the Final Rule, the SEC notes that the newly adopted principles-based conflict disclosure rule will allow a PAF to apply its judgment and unique knowledge of the facts to determine (i) the materiality of conflicts that might pose a risk to the objectivity of its advice, (ii) whether a relationship or interest that has been terminated should nevertheless be disclosed and (iii) the manner in which conflicts information is disclosed, so long as the basic requirements are met. Whether a PAF needs to disclose a conflict will ultimately be determined based on whether the information in question is material to the PAF’s objectivity.

Adoption of Written Policies and Procedures Designed to Ensure that the PAFs’ Proxy Voting Advice is Made Available to Registrants (“Delivery of Proxy Voting Advice”)

General Rule. The Final Rule also requires a PAF to adopt and publicly disclose written policies and procedures that ensure proxy voting advice is made available to each covered registrant at or prior to the time when such advice is disseminated to the PAF’s clients.

However, PAFs will be under no obligation to:

■ Allow registrants the opportunity to review proxy voting advice in advance of its distribution to the PAF’s clients (although the SEC encourages PAFs to do so to the extent feasible), or

■ Provide registrants additional versions of its proxy voting advice with respect to the same meeting, vote, consent or authorization, as applicable, if the advice is subsequently revised (however, PAFs, in their sole discretion, may provide such additional versions to registrants and they have done so in the past for larger registrants).

Safe Harbor. The Final Rule includes a safe harbor under which a PAF will be deemed to satisfy the Delivery of Proxy Voting Advice requirement if it maintains written policies and procedures that provide a registrant with a copy of the PAF’s proxy voting advice, at no charge, no later than the time such advice is disseminated to the PAF’s clients. Such policies and procedures may include conditions requiring that:

■ The registrant has filed its definitive proxy statement at least 40 calendar days (or such shorter time period, as specified in the PAF’s discretion) before the meeting, or if no meeting is held, at least 40 calendar days before the date the votes, consents, or authorizations may be used to effect the proposed action; and

■ The registrant has acknowledged that it will only use the copy of the proxy voting advice for its internal purposes and/or in connection with the solicitation and such copy will not be published or otherwise shared except with the registrant’s employees or advisers.

To qualify for the safe harbor, the terms of the acknowledgement cannot be more restrictive than in the Final Rule. However, if a PAF wishes to impose more tailored or restrictive conditions, it can do so outside of the safe harbor, provided the policies and procedures do not unreasonably inhibit timely notice to the registrant consistent with the principles-based requirements.

Adoption of Written Policies and Procedures Designed to Ensure that the PAF Provides Clients with the Registrant’s Views about the PAF’s Proxy Voting Advice (“Registrant Feedback Mechanism”)

General Rule. The Final Rule requires that a PAF provide:

“a mechanism by which clients can reasonably be expected to become aware of any written statements regarding the proxy voting advice by registrants, in a timely manner before the shareholder meeting (or, if no meeting, before the votes, consents, or authorizations may be used to effect the proposed action).”

However, the Final Rule does not:

■ Prescribe the manner or specific timing in which a PAF must obtain a covered registrant’s commentary on the PAF’s proxy voting advice; PAFs will have the discretion to choose how best to implement the principles in the new Rule and incorporate them into the PAF’s policies and procedures, or

■ Require a PAF to consider or otherwise take into account in any way registrants’ commentary on the PAF’s proxy voting advice.

Safe Harbor. The Final Rule includes a safe harbor under which a PAF will be deemed to satisfy the Registrant’s Feedback Mechanism requirement by (i) maintaining written policies and procedures that (A) reflect the general rule described above, and (B) informing clients who receive proxy voting advice when a covered registrant notifies the PAF that it intends to file or has filed additional soliciting materials with the registrant’s statement regarding the proxy voting advice and (ii) providing notice to its clients on its electronic platform or through email or other electronic means.

PAF May Develop Custom Policies and Procedures. In the release to the Final Rule, the SEC notes that PAFs may develop their own policies and procedures outside of the safe harbor to ensure that they provide clients with a mechanism by which the clients can reasonably be expected to become aware of a registrant’s written response to the proxy voting advice in a timely manner. To emphasize the foregoing, the SEC further notes that the safe harbor is not intended to become the de facto means by which the requirement of the Final Rule may be met.

Special Exclusions

The Final Rule provides that PAFs need not meet the Exemption Requirements to rely on exemptions from the information and filing requirements under the following circumstances:

■ To the extent that their proxy voting advice is based on a custom policy, or

■ If they provide proxy voting advice as to non-exempt solicitations regarding certain mergers and acquisitions or contested matters.

Proxy Voting Advice Constitutes a Solicitation under Federal Securities Law

On August 21, 2019, the SEC issued interpretive guidance clarifying that PAFs’ proxy voting advice generally constitutes a solicitation within the meaning of the Exchange Act. The Final Rule codifies this interpretative guidance by amending Rule 14(a)-1(l)(iii) to provide that the terms “solicit” and “solicitation” include any proxy voting advice that makes a recommendation to a shareholder as to its vote, consent, or authorization on a specific matter for which shareholder approval is solicited, and that is furnished by a person who markets its expertise as a provider of such advice, separately from other forms of investment advice, and sells such advice for a fee. Accordingly, a PAF’s proxy voting advice will be required to satisfy the “Anti-Fraud Provision” of Rule 14a-9, which requires solicitations to be free from false or misleading statements or omissions of material facts. A PAF’s failure to comply with the Anti-Fraud Provision could subject it to legal damages.

Failure to Disclose Certain Information in Proxy Voting Advice May be Considered Misleading

The Anti-Fraud Provision prohibits proxy statements from including any statement that is false or misleading with respect to any material fact or omit to state any material fact necessary to make the statements in a proxy statement not false or misleading. The Anti-Fraud Provision includes examples of what, depending upon particular facts and circumstances, may be misleading within the meaning of the rule.

Although a PAF may be exempt from the information and filing requirements of the proxy rules, the PAF’s proxy voting advice remains subject to the Anti-Fraud Provision because the advice is considered a form of solicitation.

The Final Rule includes an illustrative example relating to PAF’s proxy voting advice. This new example provides that a PAF’s failure to disclose material information regarding proxy voting advice, “such as the PAF’s methodology, sources of information, or conflicts of interest,” could, depending upon particular facts and circumstances, be misleading.

As the SEC noted in the release to the Final Rule, the new example “further clarifies what has long been true about the application of Anti-Fraud Provision to proxy voting advice and, more generally, proxy solicitations as a whole: no solicitation may contain any statement which, at the time and in light of the circumstances under which it is made, is false or misleading with respect to any material fact, or which omits to state any material fact necessary in order to make the statements therein not false or misleading.”

Effective Date of Final Rules

The table below shows the various effective dates of the Final Rule.

Perspective of Major Proxy Advisors

On July 22, 2020, Institutional Shareholder Services (ISS) through its President & CEO Gary Retelny expressed its view of the adopted Final Rule. Glass Lewis has yet to express its view on the Final Rule, but did issue a preliminary perspective the day before the SEC adopted the Final Rule. These views are set forth below in their entirety.

Institutional Shareholder Services

On July 22, 2020, ISS President & CEO Gary Retelny released the following statement on the Final Rule:

“While the rules adopted today may appear less draconian than originally envisioned, they nevertheless serve as a blow to institutional investors seeking to judiciously monitor portfolio companies. As Commissioner Lee noted, these rules are ‘unwarranted, unwanted and unworkable.’ Despite seemingly reducing the previously contemplated burden on proxy advisers, the new rules, coupled with the new guidance for investment advisers, will hinder investors’ ability to vote in a timely, cost-effective, and objective manner.”

“The rule, passed today along party lines, is based on the view that the provision of proxy voting advice constitutes a solicitation, a premise which we believe is inconsistent with the plain meaning of the federal securities laws. This issue was at the heart of the lawsuit which we initiated against the SEC last year and it continues to be of concern to ISS.”

At the close of the statement, ISS notes that it “will in the coming days, after careful review of the final rule and supplemental guidance, communicate with our clients regarding our assessment of today’s SEC actions.”

Glass Lewis

The day before the SEC adopted the Final Rule, Glass Lewis sent the following email to clients and subscribers:

“SEC Adoption of Rules on Proxy Voting Advice”

As many of you are aware, the SEC has announced that it will meet tomorrow to consider adopting new rules for proxy advisors and additional guidance for investment advisers on proxy voting.

Glass Lewis, of course, has been engaging with the SEC and monitoring the agency’s rulemaking process closely. We are encouraged by reports that the SEC may have heard many of you who commented and moved away from some of the most problematic aspects of its initial proposal. However, we are also disappointed that the SEC appears to be moving forward at all and may be adopting different requirements and additional guidance without having proposed and sought investors’ views on those requirements.

While we cannot comment in any detail before seeing what the SEC does, our objective throughout this process has been preserving our ability to deliver thorough, unbiased research in a timely, cost-effective manner, in order to help you vote proxies in the best interests of your clients. With that objective in mind, we will review the final rules and guidance and share further thoughts on their implications, including the timing for their implementation, once they are issued and we have had a chance to review them. If changes are required, we, of course, will be ready to assist you to make sure you can continue to vote proxies in an effective manner and in full compliance with any new requirements.”

Meridian Comments. The following discusses the potential impact of the Final Rule on registrants and PAFs.

Registrants

For registrants, the Final Rule is a significant disappointment.

Under the proposed rule, registrants would have been able to preview and provide feedback on a PAF’s proxy voting advice for up to 5 days prior to the distribution of the proxy voting advice to the PAF’s clients. A PAF would have been required to provide registrants a final notice of the PAF’s proxy voting advice prior to delivery of the advice to the PAF’s clients. The final notice would have been required to include a copy of the proxy voting advice, including any revisions to such advice made by the PAF after the review and feedback period.

The Final Rule eliminated the requirements that a PAF (i) preview its proxy voting advice to registrants, (ii) review registrant feedback on the proxy voting advice and (iii) advise registrants of whether the PAF made any revisions to its proxy voting advice based on its review of the registrant’s feedback. The Final Rule narrows the obligation of the PAF to (i) providing its proxy voting advice to registrants no later than the advice is distributed to the PAF’s client and (ii) collecting registrant feedback on the proxy voting advice and distributing same to the PAF’s clients.

Proxy Advisory Firms

The following are key elements of the Final Rule that would appear beneficial to (or not significantly onerous on) the PAFs:

■ No required preview of proxy voting advice. PAFs are under no obligation to provide proxy voting advice to registrants prior to distribution to institutional clients (although ISS allows certain registrants a review prior to publication).

■ No required review of registrant comments. Unlike under the proposed rule, PAFs are under no obligation to review registrant feedback prior to developing its proxy voting advice.

However, the additional administrative burden imposed on PAFs by the Conflicts Disclosure requirement and Anti-Fraud Provision is uncertain. Currently, ISS and Glass Lewis privately disclose to their clients perhaps their most significant perceived conflict of interest. In particular (i) ISS discloses whether a registrant purchased its consulting services and (ii) Glass Lewis discloses whether either of its owners (Ontario Teachers’ Pension Plan and Alberta Investment Management Corp.) holds a stake in a registrant that is significant enough to be publicly disclosed in accordance with a local market’s regulatory requirements” or is among the registrant’s top 20 shareholders. Certainly, other actual or perceived conflicts of interest may arise in the future. Whether the identification and disclosure of such future conflicts of interest, if any, would create a significant administrative burden or source of potential embarrassment to ISS and Glass Lewis is unknown at this time.

Under the Anti-Fraud Provision, PAFs could theoretically be required to disclose extensive details with regard to their methodology and proprietary models used to inform their proxy voting advice. Currently, both ISS and Glass Lewis make public their proxy voting policies. While the published policies are comprehensive and detailed, the policies often do not include the methodology by which ISS and Glass Lewis apply certain policies to a particular fact pattern. Further, the proxy voting policies include certain proprietary models that essentially operate as a black box from a registrant perspective. Under what circumstances the disclosure of PAFs’ methodology and inner workings of their proprietary models would be required by the Anti-Fraud Provision is not clear at this time.

We expect that ISS will continue providing draft reports to S&P 500 companies and that Glass Lewis will revise its Report Feedback Statement program in light of the Final Rule. It is worth noting that ISS already allows for all registrants to access its reports upon final publication. In contrast, currently, Glass Lewis only allows for a registrant to access a report at the time of publication if the registrant purchases the report for a substantial fee ($4,500 to $5,500 depending on a company’s index). Once the Final Rule is in effect, Glass Lewis will have to provide its reports at no cost if it operates under the safe harbor. If it operates outside of the safe harbor, Glass Lewis will likely need to reduce the fees to remain compliant with the Final Rule.

The availability of the PAF reports and the mechanisms for registrants to provide feedback will likely lead to increased scrutiny over the quantitative and qualitative components of their proxy voting recommendations and analyses. Registrants will have a stronger incentive to challenge the PAF evaluation, given that PAFs will have to implement procedures to notify investment advisers of registrant feedback and investment advisers will have to consider such information prior to exercising their voting authority. This may marginally reduce the influence of PAFs if fewer investment advisers use automatic voting mechanisms through the PAFs or regularly vote their proxies consistent with the PAF’s vote recommendations.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com