Each year, Institutional Shareholder Services (ISS) surveys institutional investors, public companies (“issuers”) and the consulting and legal community on emerging corporate governance and executive compensation issues as part of its annual policy formulation process. Issuers and their advisors are collectively referred to as “non-investors” hereafter. Possibly reflecting concerns about the influence of ISS policies, 63% of this year’s survey respondents were issuers, while only 22% of respondents were investors who generally are large institutional shareholders.

The 2018 survey focused on five areas1 of which this Client Update will focus on the following two areas: gender diversity on corporate boards and the CEO pay ratio disclosure.

Gender Diversity on Corporate Boards

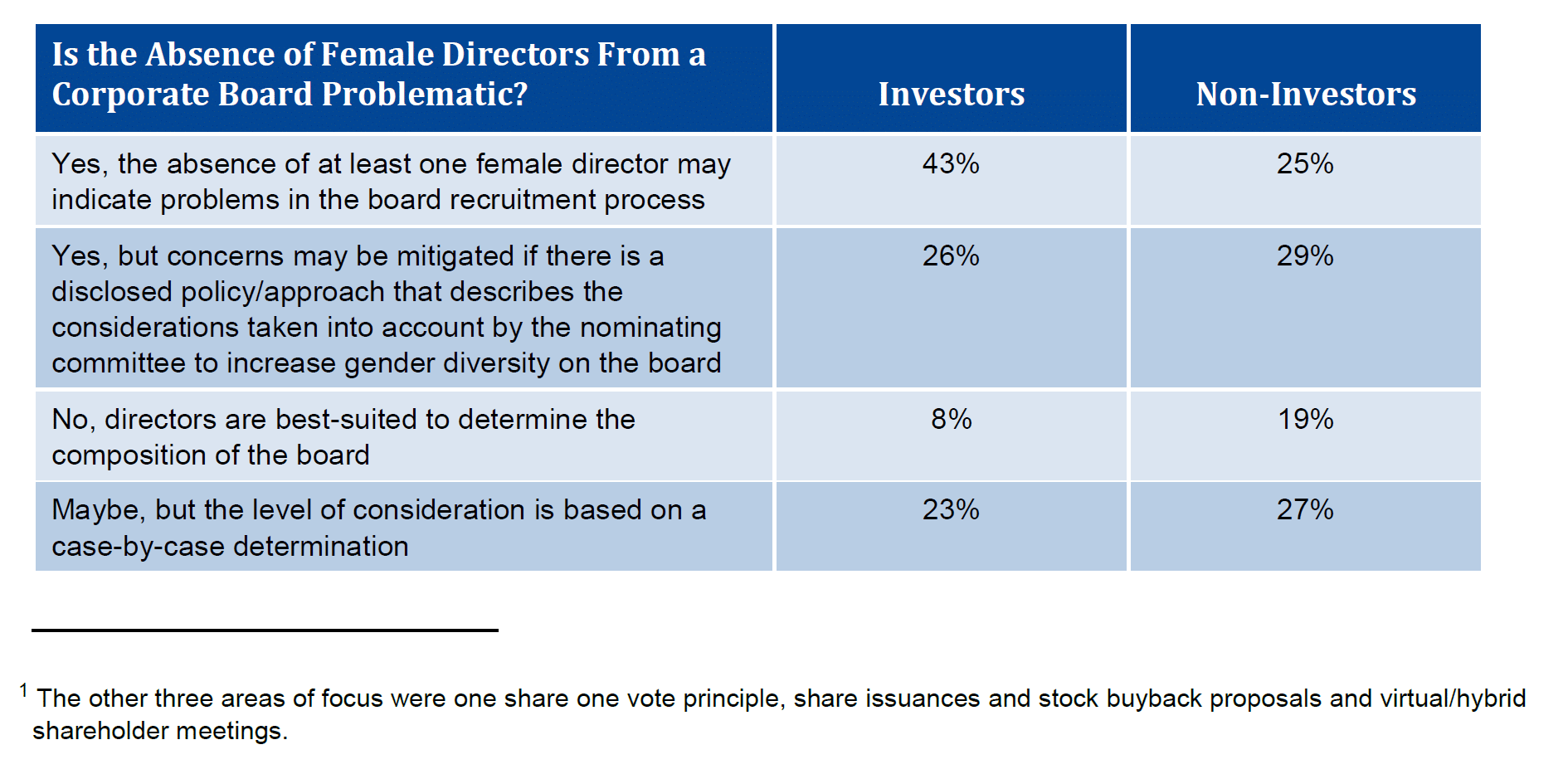

The Survey asks respondents to identify whether it is problematic for no female directors to be serving on a public company board. Both investors (69%) and non-investors (54%) believe it is problematic for no female directors to be serving on a public company board. A strong minority of investors (23%) and non-investors (27%) believe that the level of concern regarding the lack of female representation on a board should be based on a case-by-case determination. Only 8% of investors and 19% of non-investors believe that the absence of female directors serving on a public company board is not problematic.

The following chart summarizes investor and non-investor responses on whether the absence of female directors on a corporate board is problematic.

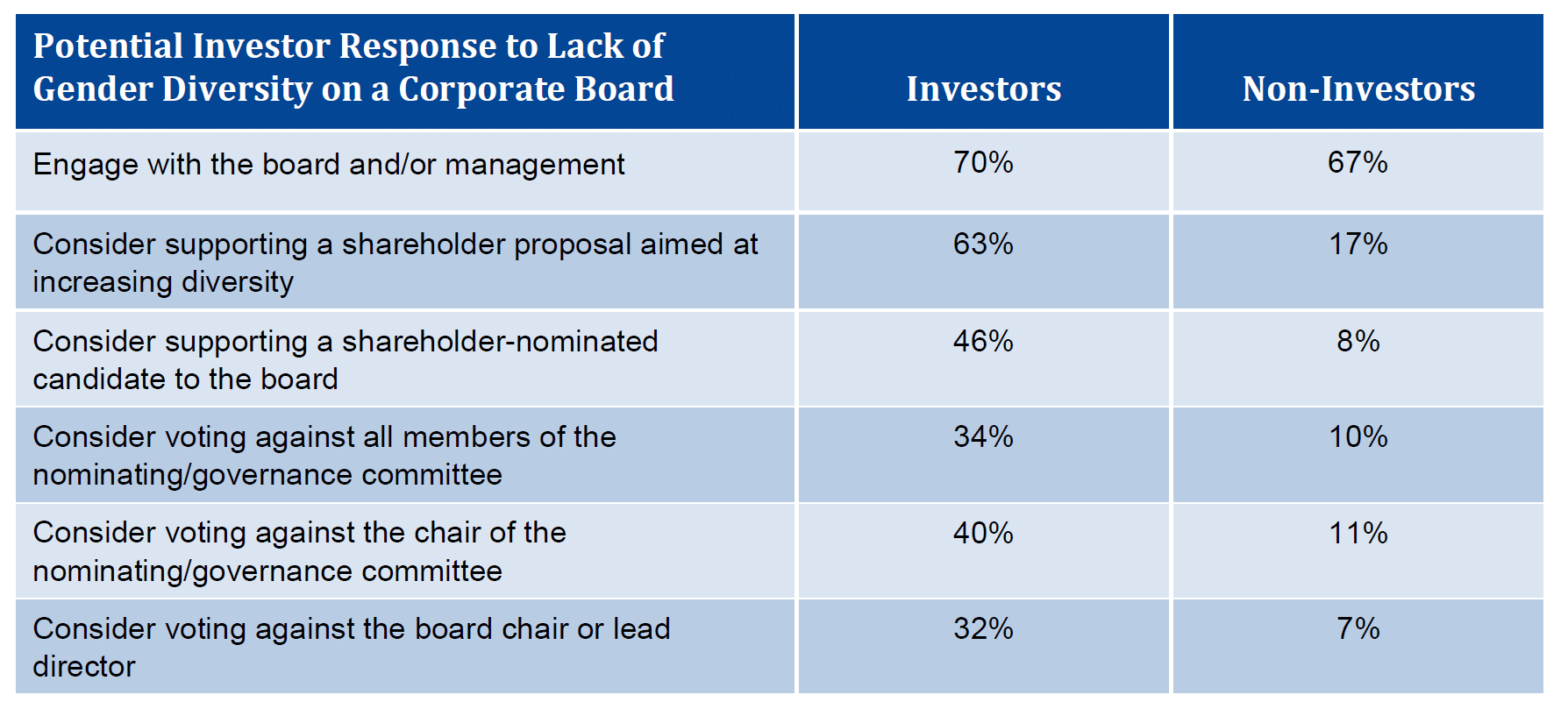

A majority of both investors and non-investors that view the absence of gender diversity to be problematic believe that shareholders should engage with a company’s board and/or management on gender diversity issues. A majority of investors also believe that shareholders should consider supporting a shareholder proposal aimed at increasing diversity (63%) and a strong minority (46%) believe that shareholders should consider supporting a shareholder-nominated candidate to the board when a company lacks any gender diversity on the board and/or has not disclosed a policy on the issue.

The following chart summarizes investor and non-investor responses on potential investor responses to lack of gender diversity on a corporate board.

Meridian Comment. ISS appears to be gauging investor interest in various mechanisms for promoting gender diversity on corporate boards. This year, investors such as BlackRock, State Street and Vanguard have focused additional resources on this issue. Nevertheless, in the near-term, we believe that ISS is unlikely to adopt a specific new policy on gender diversity. However, we expect that ISS will continue to support shareholder proposals seeking increased board diversity.

CEO Pay Ratio

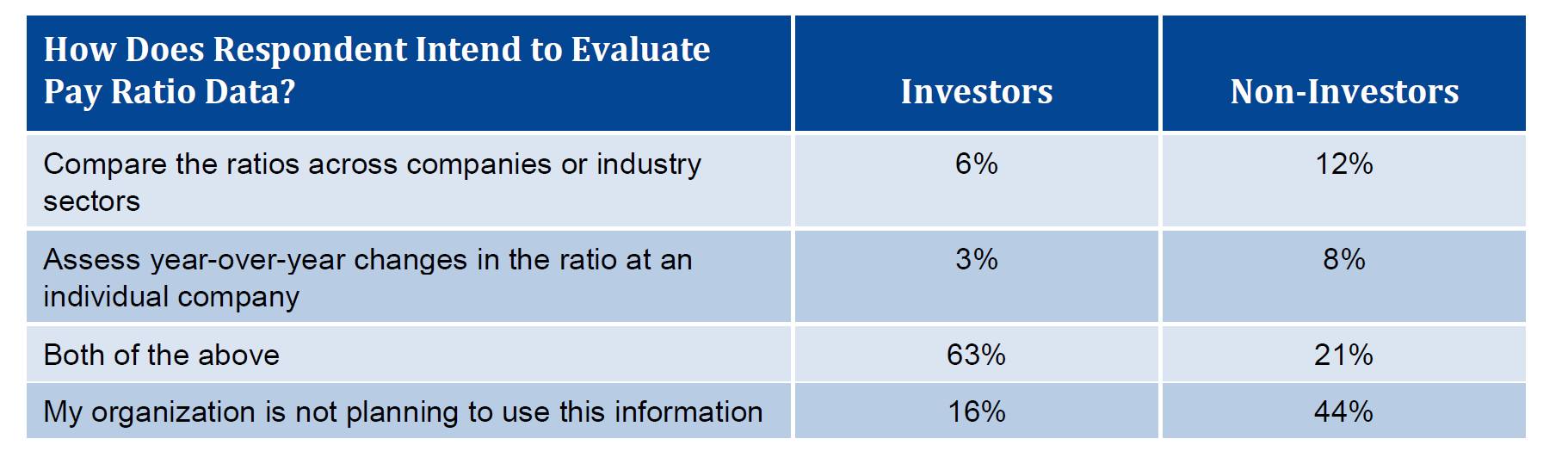

As U.S. public companies are expected to first disclose their CEO pay ratios in 2018, the 2018 survey solicited information regarding how respondents will analyze pay ratio data. Nearly three-quarters of investors responded that they intend to compare CEO pay ratios across companies or industry sectors and/or assess year-over-year changes in the ratio at an individual company. Only 16% of investors responded that they do not plan to assess or otherwise make use of the CEO pay ratio disclosure.

While a slight minority of non-investors (41%) intend to analyze pay ratio data through comparisons or year-over-year assessments, a plurality of non-investors (44%) expressed doubt about the usefulness of the information.

The following chart summarizes how respondents intend to evaluate pay ratio data.

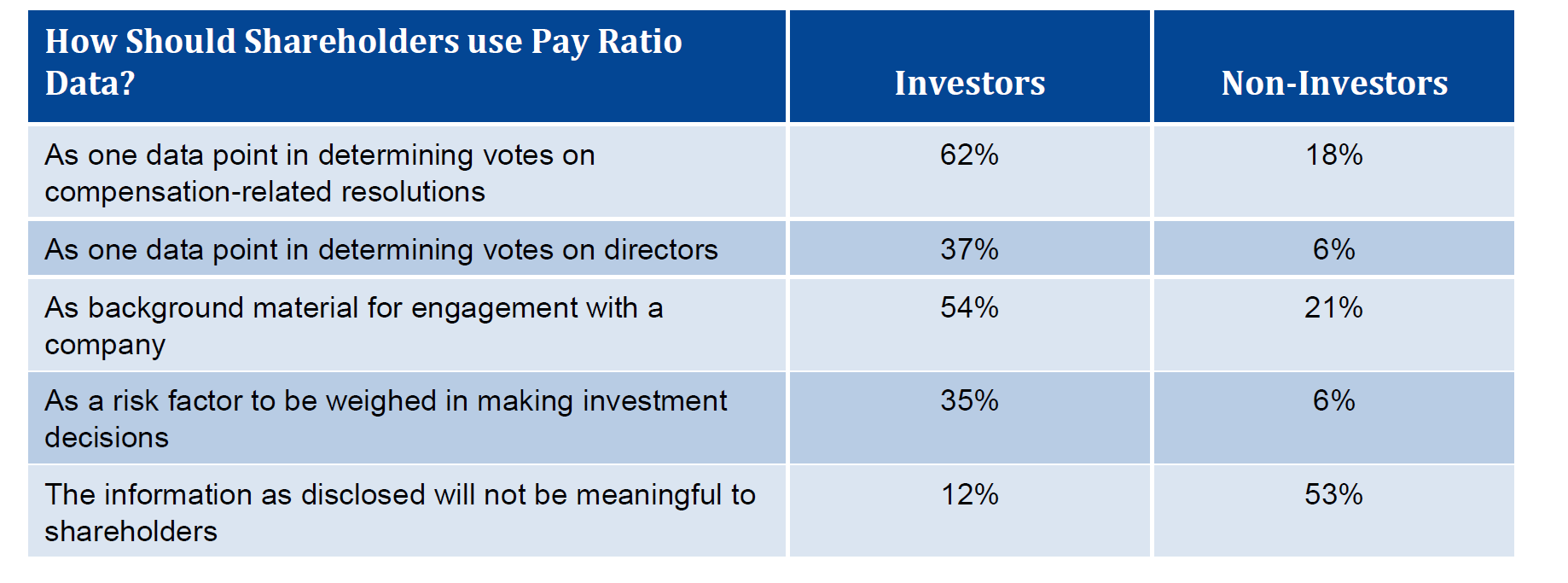

The Survey also asks respondents to identify how shareholders should use the proxy disclosed pay ratio data. A sizeable majority of investors (62%) believe that pay ratio data should be used as a data point in determining votes on compensation-related resolutions and a slight majority of investors (54%) believe that it should be used as background material for engagement with a company. In contrast, a majority of non-investors (53%) believe that the pay ratio information, as disclosed, will not be meaningful to shareholders.

The following chart summarizes investor and non-investor responses on how shareholders should use disclosed pay ratio data.

Meridian Comment. As 2018 will be the initial year for public companies to disclose their respective CEO pay ratios, ISS appears to be seeking guidance as to how it should assess this disclosure. At least for 2018, we believe that ISS will take in account the CEO pay ratio when performing its holistic analysis of a company’s pay programs. However, we do not believe that a company’s CEO pay ratio, standing alone, would result in ISS recommending AGAINST a company’s Say on Pay proposal. We further anticipate that ISS’s proxy research reports will include a company’s pay ratio information and, over time, comparative pay ratio data of peer companies.

In the future, ISS is likely to develop specific proxy voting policies on disclosed CEO pay ratios.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com