Final Policy Updates for 2018

The policy updates and guidance revise ISS proxy voting policies and methodologies for U.S.-listed companies in the following areas relating to executive compensation and corporate governance:

■ ISS quantitative pay-for-performance assessment,

■ ISS Equity Plan Scorecard evaluation,

■ Evaluation of non-employee director compensation,

■ Problematic pledging of company stock,

■ Lack of (i) Say on Pay or (ii) Say on Pay Frequency ballot items,

■ Board responsiveness to low shareholder support on a Say on Pay proposal,

■ Board diversity,

■ Director attendance,

■ Restrictions on binding shareholder proposals, and

■ Shareholder proposals related to gender pay gaps.

These policy updates take effect for shareholder meetings occurring on or after February 1, 2018.

ISS Quantitative Pay-for-Performance Assessment

ISS is modifying its quantitative pay-for-performance assessment.

Current Approach

The quantitative portion of ISS’s pay-for-performance evaluation for Russell 3000 companies includes a comparison of CEO total pay and company performance, as measured by total shareholder returns over various time horizons on both a relative and absolute basis (Quantitative Analysis). If the Quantitative Analysis shows that significant pay misalignment exists, then ISS will perform a more in-depth qualitative assessment, taking into consideration a number of unweighted factors to determine whether a company’s pay practices mitigate or facilitate the misalignment (Qualitative Analysis). Generally, ISS will perform the Qualitative Analysis in cases where the Quantitative Analysis yields a “medium” or “high” concern level regarding a potential misalignment of pay and performance. When the Qualitative Analysis shows that the pay misalignment is “facilitated by company pay practices,” ISS will likely recommend an AGAINST vote on a company’s Say on Pay proposal.

New Approach

ISS is modifying its quantitative pay-for-performance assessment in the following respects:

■ Lower threshold for “medium” concern level on the multiple of median (MOM) test. For S&P 500 constituent companies only, the threshold for a “medium” concern level on the MOM test will be reduced from 2.33× to 2.00× the ISS-developed peer group median. All of the other quantitative pay-for-performance test thresholds are expected to remain constant for 2018.

■ Calculation of total shareholder return (TSR). In calculating TSR for purposes of the Relative Degree of Alignment and Pay-TSR Alignment tests, ISS will smooth the beginning of period and end of period stock prices by averaging the closing prices for each trading day of the applicable month. The applicable month will be the month closest to the subject company’s fiscal year end. For example, if a company’s fiscal year end is on or after the 15th day of the month, then ISS will use the monthly average for that month. Conversely, if a company’s fiscal year end is before the 15th day of the month, then ISS will use the monthly average for the prior month. This change is intended to reduce the impact of point-in-time stock price fluctuations in the TSR calculation.

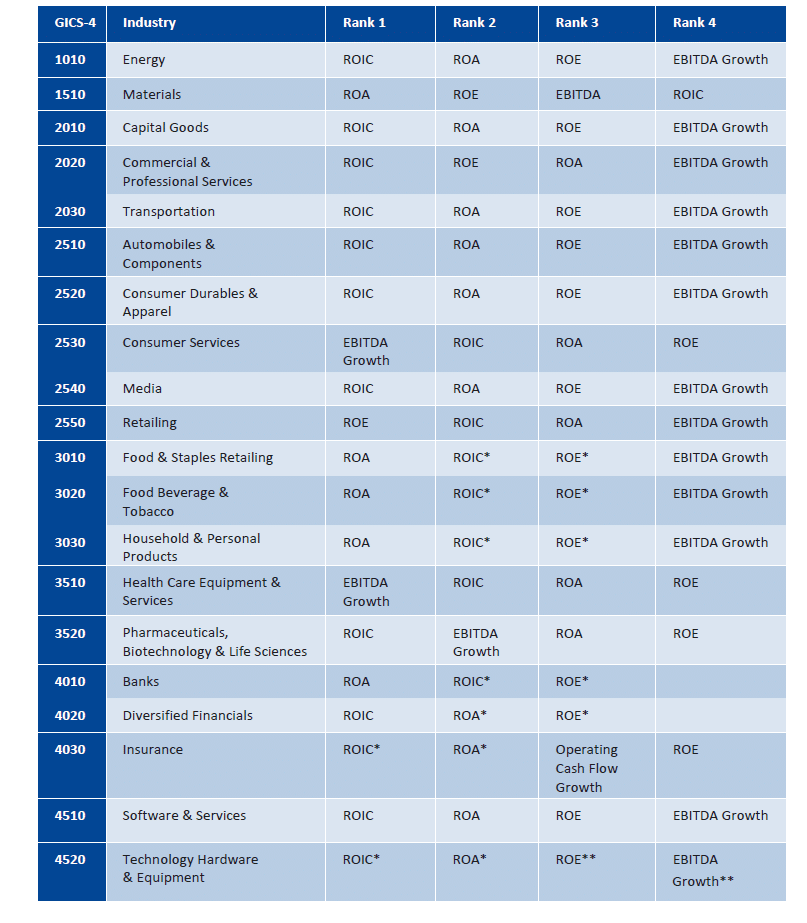

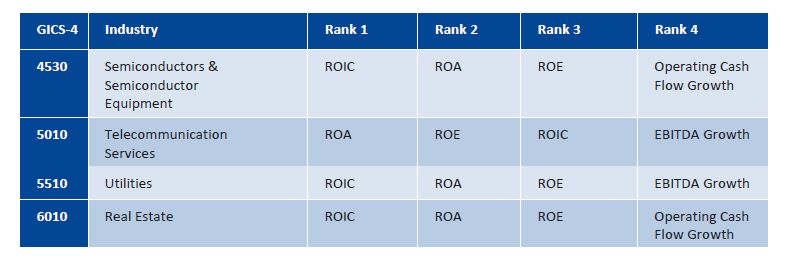

■ Use of relative financial performance analysis (FPA). As discussed in our Client Update dated October 24, 2017, for 2018, ISS will include a FPA in its Quantitative Analysis as a modifier when the existing quantitative tests yield scores near the upper threshold for a “low” concern or the lower threshold for a “medium” concern. The FPA modifier may result in some companies moving from a “low” concern to a “medium” concern and others from a “medium” concern to a “low” concern. Generally, ISS has reduced the number of financial measures in the FPA from seven metrics to four metrics for most industries (ISS will use three metrics for banks and diversified financials). For each industry, ISS will select and weigh financial metrics, which include return on invested capital, return on assets, return on equity and EBITDA growth for most industries. ISS has published a table that lists the metrics and relative weighting of each metric used in the calculation of FPA for each four-digit GICS industry (as provided in Appendix A).

ISS Equity Plan Scorecard Evaluation

ISS is modifying its existing methodology for evaluating proposals to adopt new equity plans and plan amendments that include a request for additional shares under the equity plan (Equity Plan Proposal).

Current Methodology

ISS evaluates Equity Plan Proposals under its Equity Plan Scorecard (EPSC). Under the EPSC, ISS will determine its vote recommendation on Equity Plan Proposals based on the outcome of the following three-part analysis: (i) plan cost, (ii) plan features, and (iii) company grant practices. ISS employs separate scoring models for equity plan proposals from S&P 500, Russell 3000 (excluding S&P 500), Non-Russell 3000 companies and recent IPO/bankruptcy emergent companies. This analysis yields a specific point score, up to a maximum score of 100. Generally, ISS will issue a positive vote recommendation if a company’s point score is at least 53.

Methodology Updates

ISS is modifying its policy on EPSC evaluations in the following respects:

■ Threshold point score for a positive vote recommendation. For S&P 500 constituent companies only, the threshold score for a positive vote recommendation will increase to 55 points. For all other companies, the threshold score for a positive vote recommendation will remain 53 points.

■ Change-in-control (CIC) vesting provisions. One factor ISS evaluates under its EPSC is the treatment of outstanding non-vested equity awards upon a CIC (“CIC Vesting Factor”). Under its new guidance, ISS clarifies the manner in which it will evaluate this treatment. Specifically, ISS has simplified its standard for scoring the CIC Vesting Factor, with companies either receiving full or no points for the EPSC factor. A company will receive full points for CIC Vesting Factor if the company’s equity plan contains both of the following CIC vesting provisions:

― Performance-based awards (i) accelerate in full based on actual performance, (ii) accelerate pro rata based on target performance, (iii) accelerate pro rata based on actual performance, or (iv) are forfeited or terminate.

― Time-based awards do not automatically accelerate or accelerate based on committee discretion.

In all other cases, companies will not receive any points for this factor.

■ Plan provisions allowing for broad discretion to accelerate vesting. ISS has narrowed the circumstances in which a company receives points for this EPSC factor. Under the new EPSC methodology, a company will receive points for this plan feature if the plan limits discretion to accelerate awards in the cases of death and disability only. Previously, a company would receive points for this plan feature even if the plan allowed for discretion to accelerate awards upon a CIC.

■ Post-vesting and post-exercise holding requirements. ISS has simplified its standard for evaluating holding requirements under the EPSC, with companies either receiving full or no points for the EPSC factor. The following is the new standard for scoring holding requirements.

― A 12-month holding period or holding through the end of employment will result in full points (previously, a 36-month holding period would result in full points).

― A holding period of less than 12 months will result in no points.

― A holding period that applies only until ownership guidelines are met will result in no points (previously, such a “hold until met” requirement would result in half credit).

■ CEO vesting requirements. ISS has simplified its standard for evaluating CEO vesting requirements, with companies either receiving full or no points for the CEO vesting terms of (1) time-based stock options or stock appreciation rights, (2) time-based restricted stock/RSUs, and (3) performance-based equity compensation. Each of these equity award types is evaluated and scored separately. In each case, a company will receive full points if a CEO’s equity award ratably or cliff vests at least three years from the date of grant (previously, a CEO equity award had to vest at least four years from the date of grant for a company to receive full points).

Evaluation of Non-Employee Director (NED) Compensation

ISS is adopting a new policy regarding “excessive” non-employee director compensation. The new policy will not impact ISS’s vote recommendations in 2018, as negative vote recommendations would be triggered only after a pattern of excessive NED pay is identified in consecutive years.

Current Policy

Under its current policy, ISS reviews NED compensation to determine whether a company has a pattern of excessive director compensation that calls into question director independence. However, ISS has not adopted a formal policy to issue negative vote recommendations due to excessive NED pay levels.

New Policy

Starting in 2019, ISS will generally recommend votes against members of the board committee that is responsible for appproving or setting NED compensation if there is a pattern (i.e., two or more years) of excessive NED compensation without a compelling rationale or other mitigating factors. ISS has not defined how it will determine whether NED compensation is “excessive” in its final policies for 2018.

Problematic Pledging of Company Stock

ISS has codified its existing approach of recommending against members of the committee responsible for risk overight for a signficiant level of pledging of company stock by including significant pledging activity as a problematic compensation practice that may result in negative vote recommendations on directors.

Current Policy

Under its Governance Failures policy, ISS has been recommending votes against directors individually, committee members or the full board, due to “significant” level of pledging of company stock by executives or directors, which ISS views as a material failure in risk oversight. A significant level of pledged company stock is determined on a case-by-case basis by measuring the aggregate pledged shares in terms of common shares outstanding or market value or trading volume. In determining vote recommendations regarding directors of companies who currently have executives or directors with pledged company stock, ISS considers factors enumerated in its FAQs.

New Policy

Under ISS’s new policy, ISS will recommend votes against the members of the committee that oversees risks related to pledging, or the full board, where a significant level of pledged company stock by executives or directors raises concerns. The following factors will be considered:

■ The presence of an anti-pledging policy, disclosed in the proxy statement, that prohibits future pledging activity,

■ The magnitude of aggregate pledged shares in terms of total common shares outstanding, market value and trading volume,

■ Disclosure of progress or lack thereof in reducing the magnitude of aggregate pledged shares over time,

■ Disclosure in the proxy statement that shares subject to stock ownership and holding requirements do not include pledged company stock, and

■ Any other relevant factors.

Lack of Say on Pay or Say on Pay Frequency Ballot Items

ISS has codified its existing practice of recommending votes against members of the compensation committee when a company does not include a Say on Pay vote on its ballot and does not have a legal basis for its exclusion. Similarly, ISS will recommend votes against the Say on Pay proposal or, in its absence, against members of the compensation committee if a company fails to include a Say on Pay Frequency vote on the ballot when required under SEC rules.

Board Responsiveness to Low Shareholder Support on a Say on Pay Proposal

ISS has modified its existing policy on board responsiveness to a Say on Pay proposal that received low levels of shareholder support. Specifically, ISS has clarified the factors that it will consider when assessing the adequacy of board responsiveness to a Say on Pay proposal that received low levels of shareholder support.

Current Policy

Under its current policy, if a company’s prior Say on Pay proposal received support from less than 70% of the votes cast, ISS will determine on a case-by-case basis whether the board has adequately responded to the vote, taking into account certain qualitative factors. If the board fails to adequately respond to the company’s prior Say on Pay proposal that received the support of less than 70% of votes cast, then ISS will issue negative vote recommendations on the election of compensation committee members (or, in exceptional cases, the full board).

New Policy

Under ISS’s new policy, ISS will consider the following revised list of factors when evaluating a board’s responsiveness to a company’s prior Say on Pay proposal that received the support of less than 70% of votes cast (new or revised factors noted in bold text).

■ The company’s response, including:

― Disclosure of engagement efforts with major institutional investors regarding the issues that contributed to the low level of support (including the timing and frequency of engagements and whether independent directors participated)

― Disclosure of the specific concerns voiced by shareholders that led to the Say on Pay opposition

― Disclosure of specific and meaningful actions taken to address shareholders’ concerns

■ Other recent compensation actions taken by the company,

■ Whether the issues raised are recurring or isolated,

■ The company’s ownership structure (e.g., dual class voting structure or concentrated ownership), and

■ Whether the support level was less than 50%, which would warrant the highest degree of board responsiveness.

According to its policy updates, ISS prefers independent director participation in shareholder engagements, “as it is more conducive for candid investor feedback on pay concerns (as compared to discussions with senior management about their own pay packages)”.

Board Diversity

Under ISS’s new policy guidelines, ISS has adopted a principle that a board “should be sufficiently diverse to ensure consideration of a wide range of perspectives.” To that end, ISS has revised its policy on board composition, pursuant to which ISS will identify in its reports where a board has zero female directors. However, ISS will not use any lack of gender diversity as a factor in its vote recommendations on directors.

Director Attendance

ISS has revised its policy on a newly-appointed director’s attendance at board and committee meetings.

Current Policy

Under its current policy, ISS will generally vote against a director who attends less than 75% of the aggregate board and applicable committee meetings for the period in which the director served, unless the company publicly discloses an acceptable reason for the director’s absences. For new nominees, ISS evaluates director attendance at board and committee meetings on a case-by case basis. Under the exception for new nominees, ISS considers whether the company disclosed that the new director had a schedule conflict due to commitments made prior to her appointment to the board.

New Policy

Under ISS’s new policy, for newly appointed directors, ISS has eliminated the case-by-case evaluation of attendance at board and committee meetings. Instead, new nominees who served as a director for only part of the fiscal year will generally be exempted from the attendance policy.

Restrictions on Binding Shareholder Proposals

ISS has broadened its policy on restrictions on shareholders’ ability to submit binding shareholder proposals.

Current Policy

Under its current policy, ISS will generally vote against members of the governance committee if the company’s charter imposes undue restrictions on shareholders’ ability to amend the bylaws, such as an outright prohibition on submitting binding shareholder proposals or share ownership or holding requirements that are more stringent than those required under SEC Rule 14a-8 (i.e., ownership of at least $2,000 in market value or 1% of the company’s stock for at least one year).

New Policy

Under ISS’s new policy, ISS will generally vote against members of the governance committee if any of the company’s governing documents (including its bylaws) impose undue restrictions on shareholders’ ability to amend the bylaws.

Shareholder Proposals Related to Gender Pay Gaps

ISS has adopted a policy on shareholder proposals related to gender pay gaps. Under ISS’s new policy, ISS will evaluate shareholder proposals that request reports on gender pay data or a company’s policies and goals to reduce a gender pay gap on a case-by-case basis, taking into account the following factors:

■ The company’s current policies and disclosure related to both its diversity and inclusion policies and practices and its compensation philosophy and fair and equitable compensation practices,

■ Whether the company has been the subject of recent controversy, litigation, or regulatory actions related to gender pay gap issues, and

■ Whether the company’s reporting regarding gender pay gap policies or initiatives is lagging its peers.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com

Appendix A

The following table lists the metrics and relative weighting used in the ISS relative financial performance analysis for each four-digit GICS industry.

* Indicates equal weighting for two metrics within an industry. These metrics are listed adjacently in this table.

** For GICS 4520, metrics with rank 1 and 2 are weighted equally, and metrics with rank 3 and 4 are also weighted equally but less than the rank 1 and 2 metrics.