Each year, Institutional Shareholder Services (ISS) surveys institutional investors, public companies (“issuers”) and the consulting and legal communities on emerging corporate governance and executive compensation issues as part of its annual policy formulation process (the “Survey”). Issuers and their advisors are collectively referred to as “non-investors” hereafter. Possibly reflecting concerns about the influence of ISS policies, 70% of this year’s survey respondents were issuers, while only 17% of respondents were investors, primarily large institutional shareholders.

The Survey was intended to provide feedback to ISS on a wide range of questions, including issues related to ISS’s quantitative pay-for-performance assessment methodology, non-employee director pay, gender diversity on boards, director accountability for service on other boards and the inclusion of board qualification matrices in proxies. Each of these topics is discussed below.

ISS Quantitative Pay-for-Performance Methodology (U.S. and Canada)

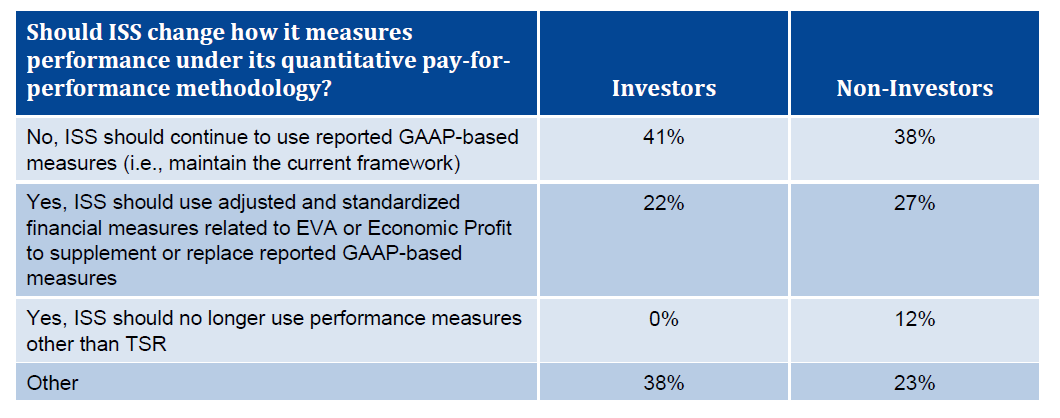

The Survey asked respondents to describe their views on whether ISS should change how it measures performance under its quantitative pay-for-performance methodology. A plurality of both investors (41%) and non-investors (38%) believe that ISS should continue to use reported GAAP measures. Only 22% of investors and 27% of non-investors believe that ISS should use adjusted and standardized measures such as EVA or Economic Profit to supplement or replace reported GAAP-based measures.

The following chart summarizes investor and non-investor responses on whether ISS should change how it measures performance under its quantitative pay-for-performance methodology.

Meridian Comment. ISS has been considering changing its methodology for assessing CEO pay and performance in the U.S. and Canada by supplementing or replacing existing GAAP-based accounting metrics with EVA-based metrics to measure corporate economic performance. A strong plurality of both investors and non-investors are in favor of ISS continuing to use reported GAAP-based measures in its quantitative pay-for-performance test. However, it remains uncertain whether (and, if so, when) ISS will change its methodology to use EVA or Economic Profit going forward.

Although many investors support maintaining the current methodology, many investors disagreed – 38% of investors responded that ISS should make “other” changes to how it measures performance under its quantitative pay-for-performance test. However, ISS did not summarize the types of changes that were proposed by those investors.

Non-Employee Director Pay

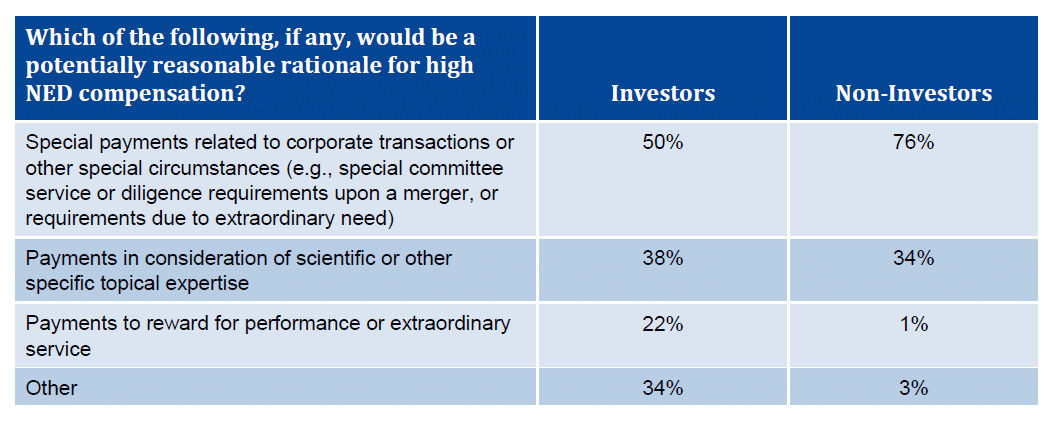

Starting with the 2019 proxy season, ISS will generally recommend shareholders vote AGAINST members of the board committee that are responsible for approving or setting non-employee director (NED) compensation if there are multiple years of “excessive” NED compensation without a disclosed compelling rationale or other mitigating factors. The Survey asked respondents to identify potentially reasonable rationales for high non-employee director compensation. Both investors (50%) and non-investors (76%) said that special payments and other special circumstances would be a reasonable rationale for high NED compensation.

The following chart summarizes investor and non-investor responses on whether the specified rationales for high NED compensation were reasonable.

Meridian Comment. Based on the survey results, ISS is likely to clarify that there are special circumstances under which it would deviate from a bright-line policy to issue negative vote recommendations due to relatively high NED pay over multiple years. In addition, at a recent conference, David Kokell, head of ISS’s U.S. compensation research team, confirmed that ISS plans to revise its director pay evaluation methodology to compare the pay of directors serving in board leadership positions (e.g., Executive Chairs, lead independent directors) to other directors serving in the same positions. Thus, ISS appears poised to provide additional details on its NED pay evaluation methodology as part of its policy updates for 2019.

Gender Diversity on Corporate Boards

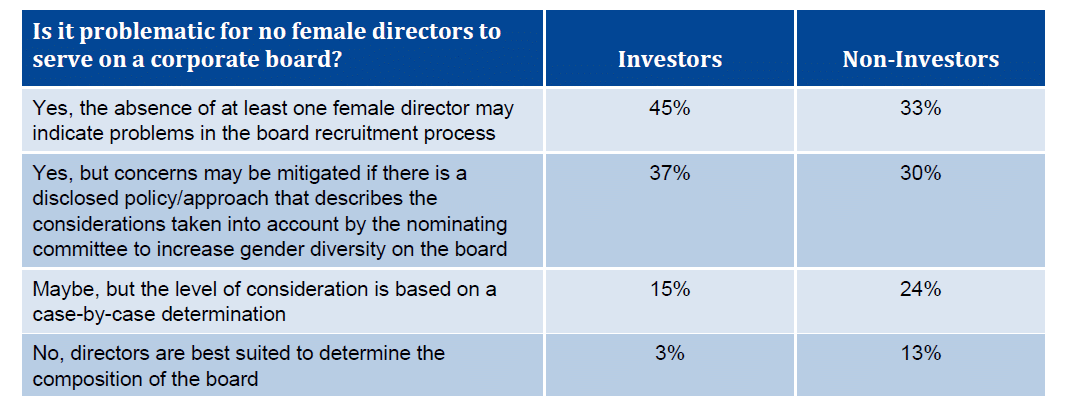

The Survey asked respondents to identify whether it is problematic for no female directors to be serving on a public company board. A majority of investors (52%) and non-investors (54%) believe that the level of concern regarding the lack of female representation on a board should be based on a case-by-case determination or based on consideration of mitigating factors. However, nearly a majority of both investors (45%) and a significant minority of non-investors (33%) believe it is problematic per se for no female directors to be serving on a public company board. Only 3% of investors and 13% of non-investors believe that the absence of female directors serving on a public company board is not problematic.

The following chart summarizes investor and non-investor responses on whether the absence of female directors on a corporate board is problematic.

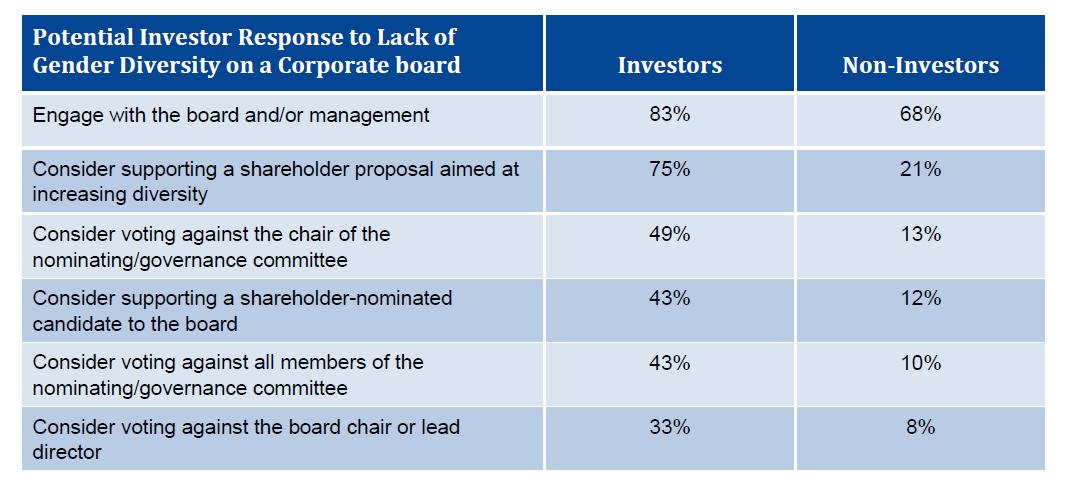

A majority of both investors and non-investors that view the absence of gender diversity to be problematic believe that shareholders should engage with a company’s board and/or management on gender diversity issues. A strong majority of investors also believe that shareholders should consider supporting a shareholder proposal aimed at increasing diversity (75%). Nearly a majority of investors (49%) believe that shareholders should consider voting against the chair of the nominating/governance committee due to lack of gender diversity, up 9 percentage points from 2017.

The following chart summarizes investor and non-investor responses on the lack of gender diversity on a corporate board.

Meridian Comment. For the second consecutive year, ISS appears to be gauging investor interest in various mechanisms for promoting gender diversity on corporate boards. Over the last two years, investors such as BlackRock, State Street and Vanguard have focused additional resources on this issue. Due to lack of majority investor support, ISS is not likely to update its 2019 policy to recommend voting against the chair of the nominating/governance committee (or all committee members) if a company’s board does not include any women directors. However, we believe it is only a matter of time until ISS eventually adopts such a policy.

Director Accountability for Service on Other Boards

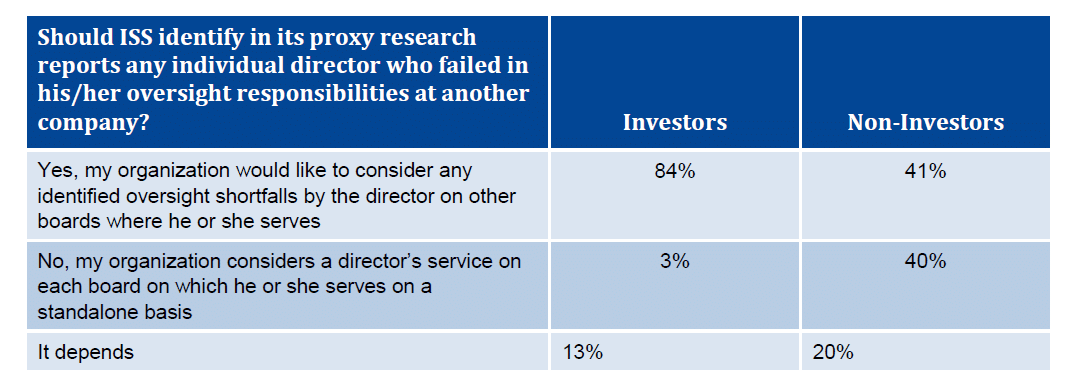

An overwhelming majority of investors (84%) said that ISS should identify in its proxy research reports any individual director who received a negative ISS vote recommendation on the basis that the director failed in his/her oversight responsibilities at another company. In contrast, non-investors were evenly split on whether information on a director’s service on another board would be useful information.

The following chart summarizes investor and non-investor responses on whether ISS should identify in its proxy research reports any individual director who failed in his/her oversight responsibilities at another company.

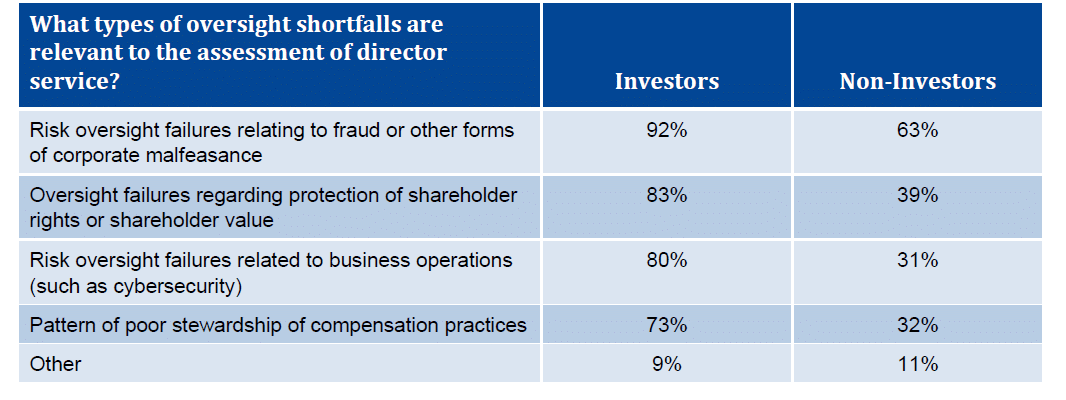

The Survey further asked respondents to identify the types of “oversight shortfalls” that are relevant to an investor’s assessment of director service. The vast majority of investors believe that all the types of oversight shortfalls specified in the Survey are relevant in an investor’s assessment of director service, including a pattern of poor stewardship of compensation practices. In contrast, a majority of non-investors found risk oversights relating to fraud and other forms of corporate malfeasance as the only relevant “oversight shortfall” in assessing director service.

The following chart summarizes investor and non-investor responses on the types of oversight shortfalls that are relevant to an investor’s assessment of director service.

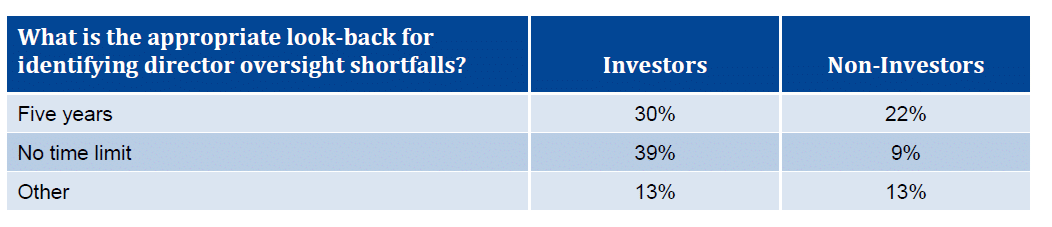

The Survey also asked respondents to determine an appropriate look-back period for director oversight shortfalls. The majority of investors (69%) believe that a five-year look-back or no time limit is appropriate, while the majority of non-investors (57%) believe that the look-back should be limited to no more than three years.

The following chart summarizes investor and non-investor responses on the appropriate look-back period for director oversight shortfalls.

![]()

Meridian Comment. This is clearly a sensitive and controversial issue. However, we expect that ISS will include information in its proxy research reports about alleged director “oversight shortfalls” on boards other than the subject company’s board. Companies should be aware of possible investor concerns about individual directors who serve on other boards.

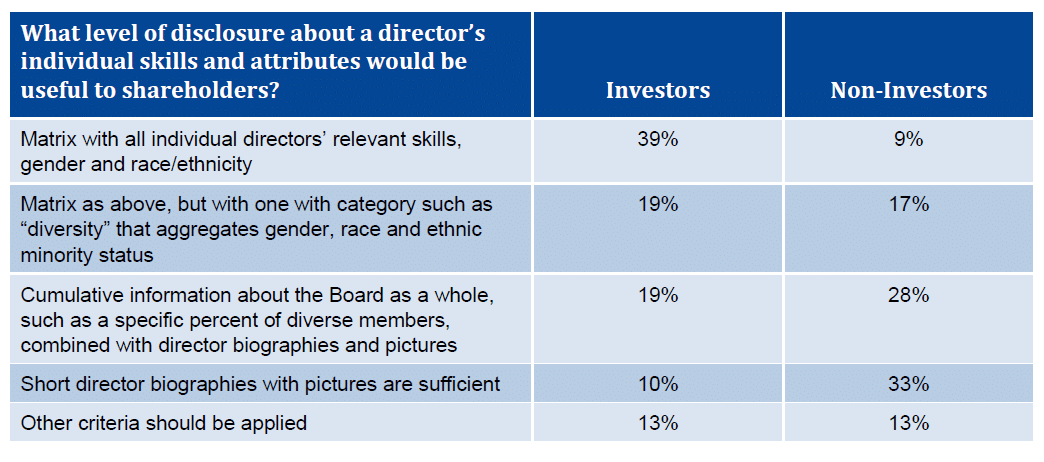

Board Qualifications Matrix

The Survey asked respondents to identify the level of disclosure about a director’s individual skills and attributes that would be useful to shareholders. A majority of investors (58%) believe that a broad matrix of directors’ skills and attributes would be useful, while a majority of non-investors (61%) believe that the current level of director biographies or director biographies and cumulative information about the board as a whole is sufficient.

Meridian Comment. The disclosure of director skills and attributes is an issue that ISS has been wrestling with over the past several years. Given the high level of investor support for enhanced disclosures and many issuers are already providing this information, we believe that ISS is likely to include negative commentary in its proxy research reports when a company does not provide adequate disclosures regarding director skills and attributes.

* * * * *

The Client Update is prepared by Meridian Compensation Partners’ Technical Team led by Donald Kalfen. Questions regarding this Client Update or executive compensation technical issues may be directed to Donald Kalfen at 847-235-3605 or dkalfen@meridiancp.com.

This report is a publication of Meridian Compensation Partners, LLC, provides general information for reference purposes only, and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

www.meridiancp.com