Chris Havey

Chris Havey

This potential wave has generated questions about Change-in-Control (CIC) severance protections, amplified by the significant coverage of Anadarko’s last minute enhancements to its CIC severance programs (see article). The Anadarko enhancements included elevated severance benefits and the re-insertion of excise tax gross-ups.

Most companies, including Anadarko, eliminated the use of excise tax gross-ups in new CIC severance arrangements, although a few grandfathered gross-up provisions still exist. Does Anadarko’s re-instatement signal a broader revival for gross-up protections? We don’t think so. We think most Boards will continue to view gross-ups as inconsistent with the Board’s disclosed policies and misaligned with good governance.

The Purpose and History of Excise Tax Gross-ups

The excise tax is a 20% additional tax applied on “excess parachute payments” under IRC Section 280G. The calculation of excess parachute payments is complicated and can be impacted by a number of variables. Until the mid-2000s, most companies simply grossed up executives for any excise taxes triggered. At the time, companies appeared to have reasonable rationale to offer gross-up protections:

- The tax is punitive – parachute payments only $1 over a “safe harbor” amount generate significant excise taxes

- Executive peers with similar compensation could face very different tax liabilities – new hires or individuals promoted in the last 5 years are more likely to trigger the excise tax

- The tax creates some undesired incentives – it encourages executives not to defer compensation and to exercise options as early as possible

- The cumulative gross-up cost can seem small compared to the total deal price – often, the total CIC packages to terminating executives (including the gross-up) are 1% or less of the overall transaction

Just over 10 years ago, proxy advisors started to recommend against director elections at companies that included gross-ups in new or amended CIC protections. The problems with gross-ups that critics have raised include:

- Higher acquisition cost – it costs the acquirer $2.50 to $3.00 to gross up every $1 of excise tax

- The perceived inappropriateness of paying an executive’s taxes

- The premium severance compensation already payable to top executives upon a CIC-related termination

- The ability to mitigate punitive taxes through a Net Best provision (the most popular approach today)

This pressure from critics and proxy advisors quickly lowered the prevalence of gross-up provisions. In Meridian’s 2017 CIC survey, the prevalence of companies that still had gross-up provisions dropped to 15%, and it is very rare for a company to add a new gross-up provision due to the likely opposition from investors and proxy advisors. Additionally, a large number of companies highlight in their CD&A that they either do not gross up for excise taxes or that they commit not to include any new excise tax gross-ups, as a matter of good corporate governance.

A Gross-Up Without Consequences?

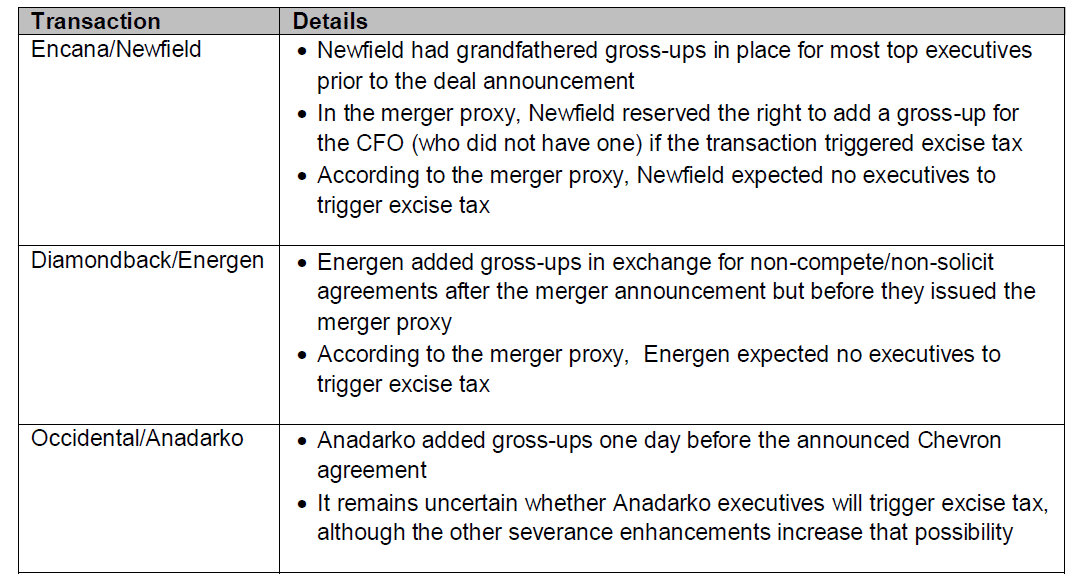

There have been a few recent industry transactions, including Anadarko’s, where the target company re-inserted gross-up protections, either for all executives or for executives who didn’t already have them.

There currently are few, if any, direct negative consequences to adding a gross-up at the time of a deal.

- Proxy advisors will likely recommend against the deal-related Say on Golden Parachute vote; however, this vote is non-binding and carries no real consequences.

- The acquired company will hold no more director elections or Say on Pay votes for shareholders to express displeasure with the action.

- Proxy advisors could recommend against the directors at elections on their other boards. Glass Lewis recently adopted a policy that it may recommend against directors for problematic actions on other boards, but it’s not clear how this policy will be applied. ISS does not currently have a similar policy, although they have mentioned adding one.

- There are usually shareholder lawsuits associated with most corporate transactions. The last-minute addition of gross-ups could provide additional fodder for litigation.

The Big Issues: Inconsistency With Prior Disclosures and Misalignment with Good Governance

While it’s possible that the last minute addition of excise tax gross-ups may not currently have many direct consequences, adopting a last minute gross-up seems inconsistent with the governance policies and messages that most Boards espouse and disclose in the CD&A. As noted above, most companies (including the three listed above prior to their acquisition) disclose in their CD&A that they do not have gross-ups or will not implement new gross-ups. Changing that policy when a deal is actually in place seems like “talking the talk, but not walking the walk”.

Finally, the re-insertion of gross-ups is simply not aligned with current good governance. In an environment where executive pay in the oil & gas industry already draws scrutiny and criticism, these examples merely add fuel to that fire. We can be certain that if this trend continues, shareholders and proxy advisors will find a way to hold directors accountable for re-insertions of gross-ups. Based on recent conversations with our oil & gas clients, we don’t expect this trend to continue.