ISS has changed its methodology for assessing treasury-based incentive plans with effect in 2016. In addition, both ISS and Glass Lewis have changed their standards for director “over-boarding” with effect in 2017.

Equity Plan Voting

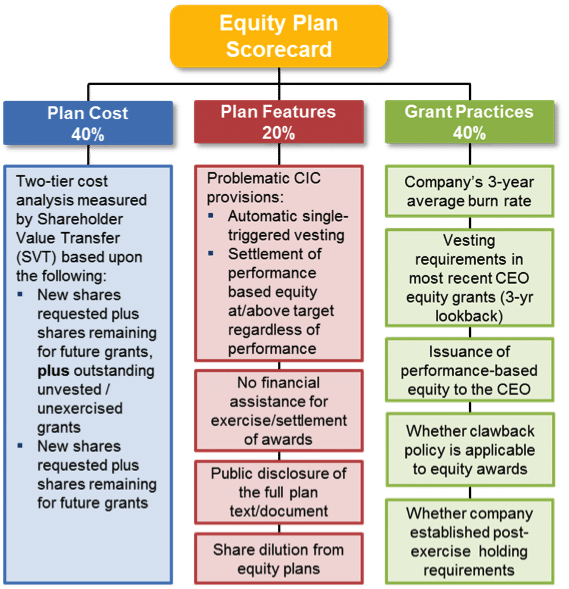

As expected, ISS is introducing to Canada the “scorecard” model introduced last year in the US for evaluating its voting recommendations on treasury settled equity plans.

ISS’s prior policy evaluated a company’s equity plan proposal using 7 governance standards. A failure to meet any of these standards would generally result in ISS recommending AGAINST the equity plan proposal (particularly, when the proposed share authorization exceeded ISS’s determined “cost” cap).

Under the new policy, starting in 2016 ISS will evaluate equity plan proposals using its Equity Plan Scorecard approach by scoring 12 separate factors that fall under one of the following 3 categories: (1) plan cost, (2) plan features and (3) company grant practices. In addition, ISS will retain existing policies on non-employee director participation, amendment provisions, a history of repricing stock options without shareholder approval, and problematic/egregious pay practices.

Under the 2015 U.S. scorecard model, a point score of 53 or higher (out of a possible 100) generally resulted in ISS recommending FOR an equity plan proposal. The vast majority of equity proposals in the U.S. did receive ISS support and high pass rates. ISS should provide more detail about how scoring will be assessed in Canada, later in December.

Director Over-boarding

Both ISS and Glass Lewis are changing the limits for directors to be considered over-boarded.

| Director Over-boarding | Current Guidelines for 2016 | New Guidelines for 2017 | |

| ISS Guidelines | Non-CEOs | Sits on more than 6 public company boards | Sits on more than 4 public company boards |

| CEO of a public company | Sits on more than 2 outside public company boards (in addition to the company of which he/she is CEO) | Sits on more than 1 outside public company boards (in addition to the company of which he/she is CEO) | |

| Glass Lewis Guidelines | Non-executive | Serving on more than 6 total boards | Serving on more than 5 total boards |

| Executive of a public company | Serving on more than 3 total boards | Serving on more than 2 total boards | |

Glass Lewis is changing its policy for 2017, and for 2016 will note as a concern where directors exceed the new 2017 limits. ISS is changing its policy for 2017 and will add cautionary language where a director is “over-boarded”, but attends more than 75% of meetings.

Other Changes for 2016

Sign-on Awards

Glass Lewis has expanded its guidelines around sign-on arrangements. These arrangements should be clearly disclosed with a meaningful explanation of the payments and how the amounts are reached, including details and basis for any make-whole payments for forfeited awards from a previous employer.

Say-on-Pay

Glass Lewis has enhanced its board responsiveness evaluation to include that compensation committees and boards should demonstrate some level of engagement and responsiveness to significant levels of shareholder opposition (defined as 25% or greater) to their say-on-pay proposal.

Externally Managed Companies

ISS will generally recommend against say-on-pay for companies with an external management structure if there is not enough disclosure for ISS to analyze pay-for-performance.

************

The Client Update is prepared by Meridian Compensation Partners. Questions regarding this Client Update or executive compensation technical issues may be directed to:

Christina Medland at (416) 646-0195, or cmedland@meridiancp.com

Andrew McElheran at (416) 646-5307, or amcelheran@meridiancp.com

Andrew Stancel at (647) 478-3052, or astancel@meridiancp.com

Andrew Conradi at (416) 646-5308, or aconradi@meridiancp.com

John Anderson at (847) 235-3601, or janderson@meridiancp.com

This report is a publication of Meridian Compensation Partners Inc. It provides general information for reference purposes only and should not be construed as legal or accounting advice or a legal or accounting opinion on any specific fact or circumstances. The information provided herein should be reviewed with appropriate advisors concerning your own situation and issues.

Meridian comment. ISS’s evaluation of a company’s equity plan has expanded beyond the requested share pool and its related cost. Through essentially a “carrot and stick” approach, ISS will increase the size of an allowable share pool provided the company adopts certain features (e.g., performance-vested CEO equity, post-exercise/post-settlement holding periods) that align with ISS’s perspectives.

Share pool authorization requests were historically focused almost exclusively on costs. We believe companies will shift towards evaluating the most appropriate plan features to adopt (while maintaining appropriate company flexibility) that also result in a meaningful share pool.

Most importantly, it will now be more difficult for a company to anticipate ISS’s likely vote recommendation without hiring the consulting arm of ISS to model the scorecard.